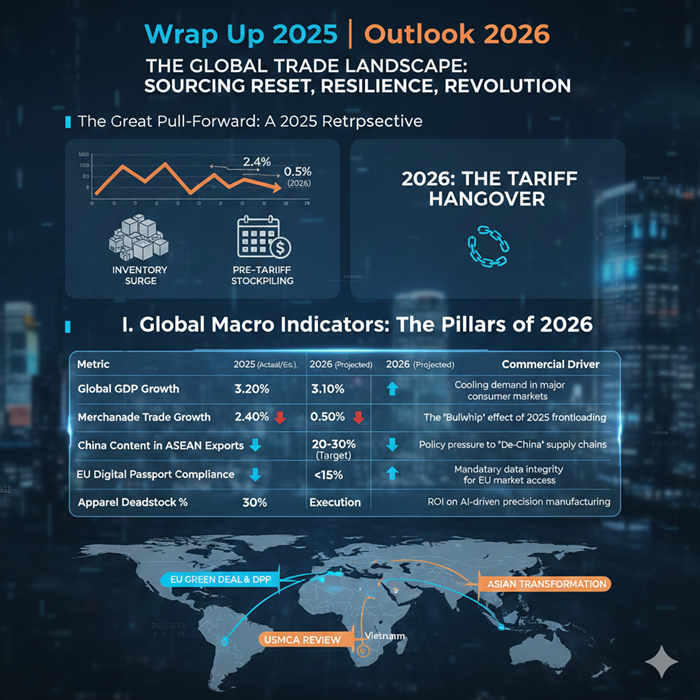

The Great Pull-Forward: A 2025 retrospective

The global textile and apparel industry spent much of 2025 in a state of hyper-vigilance. Driven by a frantic response to geopolitical volatility, importers in North America and the European Union engaged in a massive inventory "pull-forward" to insulate their bottom lines from anticipated 2026 tariff spikes and regulatory shifts. This frantic activity temporarily pushed global merchandise trade growth to a revised 2.4% in late 2025.

However, as the industry enters 2026, it faces a stark "Tariff Hangover." The World Trade Organization (WTO) has sharply downgraded the 2026 trade growth projection to just 0.5%, signaling a period of digestion where the market must work through a massive bullwhip effect of surplus stock.

I. Global Macro Indicators: The pillars of 2026

The macroeconomic backdrop for 2026 is defined by cooling global GDP growth—projected to slow to 3.1%—and a trade environment increasingly dictated by regional blocs rather than global integration. The industry has moved beyond the "China Plus One" era into a complex web of "Regional Resilience," where the winner is not the one with the lowest unit cost, but the one with the highest data integrity and landed cost predictability.

2026 Global Strategic Scorecard

II. Regional Resilience: Rewriting the global sourcing map

The 2026 trade map is being redrawn by the twin forces of protectionism and speed. While North America focuses on the high-stakes USMCA (United States-Mexico-Canada Agreement) review, the first formal six-year assessment since the pact's inception;Europe is tightening its borders through environmental mandates, and Asia is forced to innovate beyond the "China-centric" model.

Europe’s Border Control: The green deal and DPP

For the global exporter, the European Union is now a regulatory fortress. The EU Strategy for Sustainable and Circular Textiles and the Digital Product Passport (DPP) have turned data into the industry’s most valuable currency. Any product entering the EU must now carry a digital record of its environmental footprint.

"In 2026, transparency is no longer a marketing claim; it is a license to trade," notes a Brussels-based trade analyst. Suppliers in Turkey and Eastern Europe are leveraging their proximity to meet the EU's "Speed-to-Market" demands, delivering goods to hubs in just 72 hours.

Global trade corridor analysis (Turkey vs. Vietnam)

To understand the 2026 shift, one must look at the divergence between the Turkey-to-EU and Vietnam-to-EU corridors. Under the 2026 regulatory framework, the European Union's Carbon Border Adjustment Mechanism (CBAM) and DPP requirements have created a "compliance tax" on long-haul shipping.

For a standard shipment of denim jeans destined for Rotterdam, the Turkey corridor offers a total lead time of 3 to 7 days via road freight, with a landed cost that benefits from 0% customs duties under the EU-Turkey Customs Union. In contrast, the Vietnam corridor, despite the benefits of the EVFTA, faces a sea-freight lead time of 35 to 40 days. When 2026 ocean carrier emissions surcharges and the mandatory costs of RFID-enabled DPP traceability are factored in, the "unit price" advantage of Southeast Asia is often eroded by the cost of capital tied up in transit. Recent data suggests that near-shoring to Turkey or Morocco now provides 12% landed-cost savings over traditional Asian routes when accounting for these new regulatory and speed-to-market premiums.

The Asian Transformation: Beyond "China-Content"

Asia remains the engine of production, but regulators are increasingly scrutinizing the "China-content" in exports. In response, 2026 sees a massive shift toward vertical integration within Vietnam and India. India is moving into an overdrive of technical textile manufacturing, positioning itself as a high-value alternative to the volume-heavy models of the past. "The goal for 2026 is moving away from being a low-cost needle to becoming a high-tech material partner," says a lead director at the Apparel Export Promotion Council.

III. The death of the "Just-in-Case" model

The inventory glut of 2025 proved that massive stockpiles are a liability. 2026 marks the definitive end of the "Push" model in favor of "Micro-Batching." Brands are now using AI-driven demand signals to hold production back until a trend is verified, then replenishing winners in weeks rather than months.

The localized "Nano-Factory"

Localized, automated micro-hubs, or Nano-Factories;are now being deployed near major consumption centers. Startups using zero-waste algorithms to turn simple fabric rectangles into high-fashion garments. By reducing the complexity of traditional sewing, they have made local, automated production cost-competitive with offshore labor. This "On-Shoring 2.0" is about building a distributed web of high-tech hubs that can respond to the "Emotion Economy" of the modern consumer.

IV. The C-Suite Outlook: Leadership in the "Poly-Crisis"

For the modern CEO, 2026 demands a shift in identity. The "Poly-Crisis"—characterized by sticky inflation, 3.1% global GDP growth, and shifting trade alliances—requires a leader who is as much a data scientist as a creative director. The "2026 Strategic Scorecard" shows a clear bifurcation: companies that fail to specialize in either "Ultra-Fast/Ultra-Low-Cost" or "Ultra-Transparent/High-Value" are being hollowed out.

The modern CEO must recognize that the industry has hollowed out the middle; there is no longer a safe space for the "undecided" brand. Leadership is now a choice between two distinct commercial identities. On one side, the high-velocity cost leaders are doubling down on logistical efficiency and massive scale to serve a value-conscious public. On the opposite end, high-value specialists are securing their margins through radical transparency, material innovation, and circularity.

This strategic bifurcation is driven by the "Emotion Economy," where brand loyalty is earned through authenticity rather than volume. Executives are moving away from the "Attention Economy" of the 2010s to a "Loyalty Economy" that monetizes brand purpose. "In 2025, we survived the volatility by stockpiling," notes one retail executive, "but in 2026, we will survive by specializing. We are no longer just buying clothes; we are buying certainty and data-backed resilience." This shift is reflected in the massive adoption of AI; by integrating machine learning into demand forecasting, top-performing C-suites have already reported reducing their forecast errors by nearly 40%, directly translating to leaner inventories and protected margins in a stagnant growth environment.

Editor’s Conclusion: The year of verifiable precision

In 2026, a factory’s most valuable asset is no longer its sewing capacity; it is its data infrastructure. Brands are no longer just selling clothes; they are selling "Data Packages" that prove origin, ethics, and circular potential. The "Great Sourcing Reset" is complete. The industry has moved from a world of "Push" to a world of "Respond." For those leaders who have embraced AI-demand forecasting—which early data suggests has already slashed deadstock by 30%—the 2026 outlook is not one of stagnation, but of lean, profitable precision.