FW

India's apparel grew lowest in five years, says study

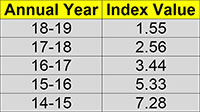

"As per CMAI's annual Apparel Index for FY2018-19, research conducted by DFU Publications on Indian apparel industry reveals, growth has been falling continuously for the past five years. In fact, except the first quarter of FY2018-19, the index values were much lower than comparable quarters in previous fiscal (FY2017-18). The Annual Index value of FY 2018-19 dipped to 1.71, the lowest ever in five years. Comparatively, the Annual Index in FY-2017-18 was 2.56; in FY-2016-17 it was 3.43 points similarly in FY-2015-16 it was 5.32 points and in FY-2014-15 it was 7.28 points."

As per CMAI's annual Apparel Index for FY2018-19, research conducted by DFU Publications on Indian apparel industry reveals, growth has been falling continuously for the past five years. In fact, except the first quarter of FY2018-19, the index values were much lower than comparable quarters in previous fiscal (FY2017-18). The Annual Index value of FY 2018-19 dipped to 1.71, the lowest ever in five years. Comparatively, the Annual Index in FY-2017-18 was 2.56; in FY-2016-17 it was 3.43 points similarly in FY-2015-16 it was 5.32 points and in FY-2014-15 it was 7.28 points. In fact, the index has been continuously falling over the years. FY2018-19 was marked by low business sentiment even during the festive season, perceived as the best time to make up for turnover losses, as buying is high at that time of year.

As per CMAI's annual Apparel Index for FY2018-19, research conducted by DFU Publications on Indian apparel industry reveals, growth has been falling continuously for the past five years. In fact, except the first quarter of FY2018-19, the index values were much lower than comparable quarters in previous fiscal (FY2017-18). The Annual Index value of FY 2018-19 dipped to 1.71, the lowest ever in five years. Comparatively, the Annual Index in FY-2017-18 was 2.56; in FY-2016-17 it was 3.43 points similarly in FY-2015-16 it was 5.32 points and in FY-2014-15 it was 7.28 points. In fact, the index has been continuously falling over the years. FY2018-19 was marked by low business sentiment even during the festive season, perceived as the best time to make up for turnover losses, as buying is high at that time of year.

The onus for fall in the last three years could be attributed to demonetization and the implementation of GST which have disrupted market sentiment and overall growth and the market has not yet recovered from their effects.

Q4 index growth dips across brand groups

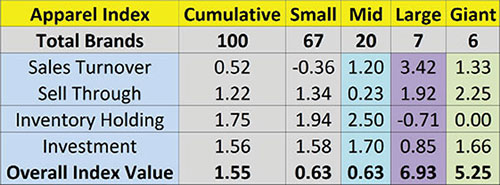

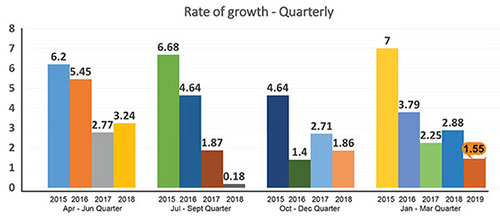

In the fourth quarter, CMAI's Apparel Index touched 1.55 points a clear reflection of low growth compared to previous quarter. In fact, Q4 (Jan-Mar FY 2018 -19) figures are lower than previous quarter’s 1.87. Like earlier, small brands sales dipped this quarter, and Giant brands at 5.25 points reported a drop in growth, compared to last quarter’s index figure of 6.00 and Q2s (July-Sept FY 2018 -19) impressive growth of 8.36. Except Large brands skyrocketing growth from 2.06 points in previous quarter to 6.93 points in Q4, all other brand groups reported a dip over last quarter.

previous quarter. In fact, Q4 (Jan-Mar FY 2018 -19) figures are lower than previous quarter’s 1.87. Like earlier, small brands sales dipped this quarter, and Giant brands at 5.25 points reported a drop in growth, compared to last quarter’s index figure of 6.00 and Q2s (July-Sept FY 2018 -19) impressive growth of 8.36. Except Large brands skyrocketing growth from 2.06 points in previous quarter to 6.93 points in Q4, all other brand groups reported a dip over last quarter.

CMAl's Q4 Apparel Index recorded a growth of 1.55 points, which is almost 2.5 times higher than the Index for Small brands (turnovers of Rs 10 to 25 crores) and Mid brands (turnover of Rs 25-100 crores) both at 0.63 points each. Large brands growth at 6.93 points, almost 4.5 times that of overall Index was the highest; at 5.25 points Giant brands’ growth is 3.38 times that of overall Index. In fact, this quarter it is the Large brands which recorded better growth. And, even though Giant brand’s rate of growth this quarter is much higher than others it is not as high as last quarter. At 1.55 points, overall Q4 index is lower than previous quarter’s Q3 Index at 1.86 points.

While Big brands (Mid, Large and Giant together) have grown at 6.08 points, much more than 3.52 points of previous quarter, individually Small and Mid brands dipped badly both to 0.63 from their previous quarter index values. Giant brands too have lost growth at 5.25 from 6.00 points previously. Only Large brands have pushed ahead to reach 6.93 (over three times) from their previous quarter’s 2.06 points.

Giant brands lost their highest growing group position to Large brands this quarter, however, both groups are still leading, outgrowing recessionary trends. Mid brands join Small brands this quarter failing to manage even moderate growth. Overall growth Index has been pulled down by these brand groups.

If Sales Turnover was to be considered as the only parameter for determining Apparel Index, this quarter then overall Index would have reflected a growth of 0.52 which is higher than previous quarter’s 0.88.

Sales Turnover down as Inventory Holding goes up

Cumulative Sales Turnover in Q4 is 0.52 a figure that is much lesser than that Q3’s 0.88. Around 39 per cent brands reported an increase in Sales Turnover this quarter compared to 48 per cent in previous quarter. “The decrease in sales turnover was mainly due to a slowdown in business due to a slowdown in the market post-Diwali. There was a substantial decrease in demand also,” explains Paresh Dedhia, Owner, Dare Jeans. On the contrary French menswear brand Celio reported positive sales turnover as Satyen Momaya, CEO, Celio points out, “The increase in sales turnover was due to our quality and we worked on an auto replenish model across our channels.” Similarly, lifestyle brand Monte Carlo gave a positive feedback as Mayank Jain, General Manager for the brand explained, “The reason for an increase in the sales turnover is we had a strong and good winter. Weather conditions were good and winter lasted for a longer period.” Adds Shitanshu Jhunjhunwala, Director, Turtle, “The increase in sales turnover was due to better work allocation. We had better sizes and availability of these sizes.”

brands reported an increase in Sales Turnover this quarter compared to 48 per cent in previous quarter. “The decrease in sales turnover was mainly due to a slowdown in business due to a slowdown in the market post-Diwali. There was a substantial decrease in demand also,” explains Paresh Dedhia, Owner, Dare Jeans. On the contrary French menswear brand Celio reported positive sales turnover as Satyen Momaya, CEO, Celio points out, “The increase in sales turnover was due to our quality and we worked on an auto replenish model across our channels.” Similarly, lifestyle brand Monte Carlo gave a positive feedback as Mayank Jain, General Manager for the brand explained, “The reason for an increase in the sales turnover is we had a strong and good winter. Weather conditions were good and winter lasted for a longer period.” Adds Shitanshu Jhunjhunwala, Director, Turtle, “The increase in sales turnover was due to better work allocation. We had better sizes and availability of these sizes.”

Almost 25 per cent brands reported a loss in Sales Turnover compared to 26 per cent in previous quarter. Except Large and Giant brands, other two groups this time reported sales losses. “The reason for the decrease in sales turnover was mainly due to closure of our stores,” observes Shyam, President 109° F.

Sell Through recorded an Index growth of 1.22 this quarter compared to 0.96 of previous quarter, still showing pressure on fresh good sales. Maximum growth in Sell Through was reported by Giant brands. Mid brands however, clocked in the lowest value of 0.23. As Shyam opines “The main reason for decrease in sell through is the online business has taken over a lot and has hampered business. It has actually killed it.”

Nearly 49 per cent brands reported an improvement in Sell Through, higher than 46 in Q3. “The major reason for an increase in sell through is the discounts given by brands before season and comparative price of the product. Imports from China is also a factor,” opines Rakesh Jain, CEO, Miss Grace.

Inventory Holding in Q4 is 1.75 points, this is higher than 1.6 points in Q3. Almost 61 per cent respondents across brands said their Inventory Holding moved north this quarter higher than 58 per cent in Q3, a very high number and they were responsible for pulling down overall apparel index value. Increase in Inventory Holding impacts overall index negatively. Higher Inventory Holding indicates more stocks in warehouses or shop shelves. Maximum increase in Inventory Holding was among Mid brands causing low index value; Giant brands on the other hand showed zero change in Inventory Holding. As Deepak Singhla, Marketing Head of Cantabil says “The decrease in inventory holding was because there was an increase in sale. Stock also sold off easily as well.” Agreeing on this point Jain says “Inventory holding decreased as store level sales have gone up, hence, there was no dead stock.”

However as per Momaya, “Inventory holding has actually not increased but has moved. There was more productivity and hence, inventory holding has gone down due to replenishment schemes.” However, Dedhia points out, “Increase in sales turnover and increase in inventory goes hand in hand. Payment cycles have stretched. There is less rotation of funds in the market.”

Investments, however, are low for the overall apparel segment, fresh Investments decreased to nearly 1.56 points, as against 1.62 points last quarter. Highest investments were done by Mid brands followed by Giant brands. Overall nearly 73 per cent respondents reported a rise in investments which is lower than 81 per cent in previous quarter. High investments in last quarter indicate most brands had to invest to manage albeit small growth which means growth is not coming easily.

An average outlook for next quarter

Around 58 per cent (last quarter 52 per cent) brands say the outlook for next quarter is ‘Average’. Generally, Q1 of the new fiscal, should be better as fresh summer sales picks up and prior to EOSS in July. However, there is no such excitement as the market has still not recovered from the earlier slowdown. Another factor could possibly be the Lok Sabh elections in Q2 this year which may have resulted in tepid response.

CMAl’s Apparel Index

CMAl’s Apparel Index aims to set a benchmark for the entire domestic apparel industry and helps brands in taking informed business decisions. For investors, industry players, stakeholders and policymakers the index is a useful tool offering concrete and credible information, and is an excellent source for assessing the performance of the industry. The Index is analysed on assessing the performance on four parameters: Sales Turnover, Sell Through (percentage of fresh stocks sold), number of days of Inventory Holding and Investments (signifying future confidence) in brand development and brand building.

The Apparel Index research is conducted by DFU Publications.

US/UK consumers expect brands to focus more on sustainability: Study

Consumers in the UK and the US want the fashion industry to become more sustainable. They now try to keep clothes longer because it’s better for the environment and are willing to pay more for sustainably-made versions of the same items, reveals a survey by e-commerce personalisation and retail AI platform Nosto. Consumers want retailers to clearly label clothes that are made in sustainable ways, offer discounts on clothing ranges that are more sustainable, do more to advertise and promote clothing that is made in sustainable ways, allow online shoppers to trade-in their used clothes for discounts on new items and automatically show people more sustainable alternatives to the items they are viewing online..

The survey reveals consumers also want fashion companies to reduce the amount of packaging, provide fair pay and good working conditions, use renewable and recyclable materials, make clothes that are designed to last longer and use fewer resources e.g. power, water, materials. But although brands are aware that consumers are increasingly concerned about sustainability in the fashion industry, they need to be more transparent and get better at communicating how they’re addressing it. The problem lies in knowing which fashion brands are really committed to sustainability. And consumers say it is difficult to know what fashion brands mean when they say they are committed to sustainability.

Sutlej Textiles expands capacity with new projects

Sutlej Textiles and Industries is expanding capacity through several new projects. The company is implementing a green fibre project to manufacture polyester staple fibre (PSF) by recycling of pet bottles at Baddi in Himachal Pradesh. The company has commenced work on the manufacturing of raw white & black recycled fibre with capacity of 120 MT/day. The total project cost is around Rs. 189 crores, and commercial production is expected to start in Q1 of FY20-21. The new plant will fulfill 75 per cent of Sutlej’s captive requirement of PSF, which is the key raw material.

Sutlej has also been continuously modernising its existing plant. The company invested around Rs 38 crores during FY19 towards technology upgradation and debottlenecking, etc. This will result in further improvement in efficiency and sustaining plant utilisation. Nearly 32 per cent of the spindleage and 67 per cent of the fabric weaving machines have been commissioned in the last decade, assuring high technological relevance.

To enhance its portfolio and presence in the home décor segment, Sutlej acquired American Silk Mills (ASM). The company is strengthening its product portfolio by leveraging the ASM design expertise and US presence, focussing on higher end markets in developed counties, building world-class design capabilities and improving product mix and broadening product portfolio.

Santoni’s introduces new seamless circular knitting machines

Italy-based textile machinery company Santoni has come up with seamless circular knitting machines, together with sock knitting machines, large diameter fabric knitting machines, and process finishing technology. Added to these are the brand new, patented X Machine and XT Machine with their ingenious intarsia technology, a new automatic finishing system for seamless boxers, and the innovative K Fabric Project that introduces a completely new type of knitted textile process. The TC Cut machine is a round-shape toe closer with an integrated slitting device to prepare stockings for manual assembly.

Santoni was founded in 1919 as a socks machine manufacturer. It is now a leader in the production of electronic machines for garments without seams and caters to manufacturers of underwear, sportswear, beachwear, medical wear, denim wear, smart textiles, socks and footwear.

Mec-Mor machines are equipped with needle-shifting movement of the needle beds. This technology enables the production of weft double-face knitted garments with high quality designs and record production times. It is also used to produce accessories, such as 3D backpacks, where various yarns can be knitted into ad-hoc positioned areas, in order to obtain a seamless structure that guarantees superior product performance. The SM8-TOP2V cut and sew machine applies a gusset into each boxer with a four-needle sewing head, completing the whole process automatically and offering the finished boxer ready for the final packing stage.

North Indian farmers return to cotton

Farmers in North India have made a comeback to cotton this year. The fiber crop helped growers across the country get decent prices last year. So, sowing in Punjab and Haryana is expected to increase by about 10 per cent. In Punjab, cotton acreage has increased by around 41 per cent, to about four lakh hectares this year over the previous year, while the growth in acreage in Haryana is around five per cent, at 6.35 lakh hectares.

Untimely rains in the month of May in Punjab and Haryana did impact planting and force farmers to resow patches. However, cotton sowing prospects in other regions will depend on multiple factors such as the monsoon as well as alternate crops such as castor and soybean. Farmers have multiple alternates available for cotton. So they will opt for the higher return crop especially when there is still an uncertainty over the monsoon. Despite the crop size being smaller than the previous year’s, the prices supported by higher MSP have given better returns to cotton growers. While it is premature to estimate the sowing prospects in central, western and southern India before the onset of the monsoon, there is an optimism about the cotton crop this year.

Western Hemisphere emerges alternative sourcing destination for US denim apparels

The Western Hemisphere is becoming an important alternative to Asian sourcing, particularly in light of the US-China trade war and the threat of 25 percent tariffs on jeans imports from the country. According to the Commerce Department’s Office of Textiles & Apparel (OTEXA), denim apparel imports from the Western Hemisphere increased by 13.41 per cent in the first four months of the year to reach a value of $323.68 million. This represented a 27.4 per cent market share of all U.S. imports of denim apparel, 97 percent of which is jeans. The market share gained 8.17 percent for the year through April.

Countries such as Mexico, Nicaragua and Guatemala are leading growth in the region as a more local, faster-turn and generally duty-free option to sourcing from the Asian production giants like Vietnam, Bangladesh and Pakistan. Nicaragua’s jeans shipments to the U.S. jumped 23.57 percent in the period to $32.38 million, while imports from Guatemala rose 36.58 percent to $10.77 million.

The two countries are part of the Central American Free Trade Agreement (CAFTA), which allows duty-free treatment under certain input stipulations and has boosted exports for U.S. yarn and fabric manufacturers. Jeans imports from the CAFTA countries rose 26 percent to $43.75 million in the first four months of the year compared to the year-ago period.

Chinese polyester plants scale down

From April to May, many polyester plants in China scaled down or suspended production. Polyester feedstock price also weakened. The inventory burden has been obviously eased. Cash flow of PFY and PET bottle chips slightly improved, and PFY plants turned to be profitable but PSF plants still suffered losses with falling prices. The polymerization rate has increased to around 90.5 per cent from 87.8 per cent. In addition, some PFY and PSF plants have presold some orders. The polymerization rate is expected to be supportive to the upstream feedstock market in the short term.

Players lowered their run rate to slow down the accumulation speed. Orders improved sporadically after PFY price firmed up, but the overall weakness has not changed, supporting the run rate of twisting units and fabric manufacturing plants. The intensified Sino-US trade conflict has made downstream plants cautious in purchases and the situation is not expected to change in the short run.

Replenishing of downstream plants in June has improved compared with April or May. Polyester plants witnessed decreasing stocks. Actually, the inventory was transferred to the downstream market and partially to traders. Downstream demand has been continuously weak. Stocks of feedstock and finished goods are expected to be high in the short run.

Child labor plagues supply chains

Child labor is still prevalent in global supply chains. This is true of manufacturing hubs like Bangladesh, China, Cambodia and Vietnam. So says research consultancy Child Labor Index, which first began compiling comparable data in 2016.

Nearly f 27 out of 198 countries—accounting for more than 10 per cent of the world’s population—were found by the index to pose an extreme risk, with North Korea, Somalia and South Sudan the top three worst offenders. Ethiopia, Bangladesh Turkey and Vietnam reveal no change in their high risk of children being exploited or forced to work out of necessity. Venezuela saw the highest risk in child labor risk. However, 52 countries registered significant improvements between 2017 and 2019. Those include Liberia, Myanmar and Madagascar.

Child labor is defined as employment that limits or damages the physical, mental, moral, social or psychological development of children. Assuming the minimum age for work is 15, there are roughly 150 million child laborers around the world, particularly on farms in Africa and Asia. The economic momentum of many countries is yet to trickle down to the poorest in society and any meaningful headway on labor rights issues, including child labor, remains elusive.

China exporting goods to the US through Vietnam

Goods are arriving in the US claiming to be made in Vietnam while they are in fact made by Chinese companies. They are indulging in this practice to avoid high tariffs. Many of them have shifted production from China to Vietnam to avoid the 25 per cent levy imposed by the US on Chinese goods amid a spiraling trade war.

Dozens of fraudulent product-origin certificates have been discovered on goods including textiles, fisheries, farm products, tiles, honey, iron, steel and plywood. Chinese plywood was discovered being shipped to America through a Vietnamese company. Vietnam says the trend has affected the reputation of its businesses and goods. The country has threatened to crack down on Chinese companies illegally using made in Vietnam labels on goods shipped to the US to avoid high tariffs.

Vietnam has long been a manufacturing hub for cheaply-made goods from Adidas sneakers and H&M dresses to Samsung smart phones and Intel processors. Those exports have soared this year as China and the US have escalated tit-for-tat tariffs on billions of dollars worth of goods. In the first three months of this year, US imports from Vietnam rose 40 per cent from the same period last year.

Birla Cellulose does product mapping

Birla Cellulose has completed a life cycle assessment (LCA) of products in its portfolio. The LCA exercise has assessed the environmental footprint and its effects on human and animal health and the environment, such as ozone layer depletion, mineral use and use of nitrogen and phosphates.

A member of the Sustainable Apparel Coalition, Birla Cellulose uses the Higg Index Tool to monitor manufacturing units’ performance on environment and social scales. The index monitors energy and water consumption, reduction in effluent discharge and transport distance. For all 11 of Birla Cellulose’s manufacturing units, Higg scores have been completed along with a benchmark analysis.

Birla Cellulose works with global brands to drive initiatives to trace the source of raw materials and help them trace their complicated supply chains in India. From Forest to Fashion is the first supply chain mapping project of its kind in the apparel industry. It has provided clarity on value chain sourcing from India and improved transparency of different players involved in the supply chain of some major brands. The next step will be to digitise the entire process. Birla Cellulose is now focusing on projects within the supply chain to reduce resource use, especially water and chemicals, in different stages of the Forest to Fashion process.