FW

Pakistan may abolish zero rating on leather, garments and carpets

Pakistan plans to abolish zero-rating for exports of leather, surgical, sports goods and carpet and garment sectors. The textile sector says this is a disastrous decision which will result in the closure of small and medium units and also pull down exports from the five sectors by 30 per cent a year, hit industrial manufacturing aimed for export purposes, stimulate a flight of capital abroad and scale down manufacturing that would eventually lead to a decline exports. Overall liquidity from manufacturing of the goods to their exports is expected to get stuck. Exporters say their tax refund claims haven’t been cleared and that additional sales tax deductions would increase the amount of pending refunds and result in a financial crunch for them. The tax refund period is now estimated to be six months, hence refunds before six months are unlikely.

Pakistan is under immense pressure from the International Monetary Fund to remove tax exemptions to increase revenues. The Fund wants Pakistan to withdraw the facility in the forthcoming budget as part of the deal. Both the IMF and Pakistan are of the view that the facility has been misused by the industry to steal sales tax on their domestic sales.

Germany to host Neonyt in July, future issues facing fashion industry in focus

Neonyt will be held in Germany, July 2 to 4, 2019. This will feature women’s wear, men’s wear, children’s wear, performance apparel, shoes, accessories, jewelry and beauty. With a good balance of leading brands and newcomers, the trade show is presenting exciting labels that are dedicated to the future issues facing the fashion industry and reflect a sustainable lifestyle.

Neonyt will discuss the severe repercussions of fashion production on the planet and people. The spotlight will be on the enormous consumption of resources by the fashion industry with water continuing to be the focal topic for 2019. Neonyt will showcase solutions for sustainable fashion production, presenting trailblazing labels with innovative concepts and contemporary collections and letting international forward-thinkers have their say. In addition to the focal topic of water, questions and recommendations for action regarding the retail sector are also on the agenda.

Worldwide, the sale of clothing has doubled in the last 15 years. The huge production volume of fast fashion is linked to the industry’s enormous water consumption. It takes up to 2,700 liters to produce one T-shirt. The annual water volume consumed by the fashion industry is nearly enough to fill a total of 32 million Olympic-sized swimming pools, making it one of the most water-intensive industrial sectors.

Mills team up with brands at New York Denim Days

New York Denim Days was held June on 8 and 9, 2019. It was proof of denim’s far-reaching appeal. Yoga sessions, children’s fashion shows and one-of-a-kind goods made by indigo artisans drew an energetic crowd to the annual event. Attendees could shop and meet the makers behind the jeanswear industry.

Denim mills teamed up with brands to highlight the unique qualities of their garments. Candiani Denim presented Blue of a Kind, the upcycled premium denim brand from Italy that it recently partnered with for a jeans collection made with fabric samples. Bossa teamed with Upcycle, a recycled T-shirt company, to create a screen printing workshop. Attendees designed tees and totes made with recycled plastic bottles.

The weekend was also packed with special events, including musical acts and a speaker series hosted by Advance Denim. Topics spanned denim influencers to cotton trends. Tencel co-hosted two outdoor yoga sessions with Athleta to showcase the active wear brand’s performance denim. Participants received a free denim yoga mat and a bag made in collaboration with Naveena Denim. A children’s fashion show on the first day presented shoppable looks by brands like OshKosh B’gosh, Indi-Kids and Trico Fields. On the second day, students from the High School of Fashion Designs strutted their creations made with re-purposed denim jackets.

Ongoing Kingpins New York focuses on sustainability and heritage in denim

Kingpins New York is on from June 12 to 13, 2019. The trade show is focusing on sustainable development and heritage within the denim market. Kingpins is committed to pushing the denim industry toward a better future. A prequel to the show featured experts from brands such as G-Star and Wrangler mixed with manufacturers, fabricants, chemical engineers and technology experts. G-Star is a pioneer of responsible production with its Raw aesthetic, 3D engineered ergonomic denim innovations, a circular design, and a transparent supply chain data. It is the first denim brand to use dyes made from upcycled plant waste. Wrangler’s foam dyed denim not only reduces water use by 100 per cent, but energy and waste by 60 per cent each. Soorty has unveiled the world’s first waterless garment dyeing technology.

Indigo is the king of denim and has been around for 6000 years. Images of dyes bleeding into rivers and an inundation of data on its chemical composition and toxic byproducts have put the denim industry on high alert. It takes 2000 gallons of water to make one pair of jeans. Fifteen per cent of fabric intended for clothing ends up on the cutting room floor of which 85 per cent goes to landfills.

Indonesia to develop digital fashion platform Fitting Room

Indonesia is developing Fitting Room, a digital platform to support the fashion industry by connecting material suppliers, designers, tailors and the industry. In addition to integrating the fashion industry’s supply chain, this platform will provide convenience to consumers in buying fashion products according to their size, without having to come to tailors. Indonesia’s strategy is to participate in Industry 2.0. This refers to automation and data exchange, driven by internet advances in the manufacturing sector. The hope is to encourage small and medium sized fashion enterprises to implement this.

Indonesia’s exports of fashion products went up 7.75 per cent in 2018 compared to 2017. The country’s textile and apparel industry grew 18.98 per cent in the first quarter of 2019. This performance exceeded Indonesia’s economic growth of 5.07 per cent in the same period. The industry is supported by a structure that has been integrated from upstream to downstream, and the products are also known to be of high quality in the international market. With economic growth, and a shift in demand from basic clothing to functional clothing, such as sportswear, the national textile industry is building production capabilities and increasing economies of scale in order to meet the demand in domestic and export markets.

Inditex Q2 gross margin up six per cent

Inditex gross margin grew six per cent year-on-year to 59.5 per cent in the second quarter, as foreign currency effects moved back into favor after two years of nibbling away at profitability. Sales were up five per cent. The company bounced back from a weak start to 2019. Unseasonably cold weather in Southern Europe had stifled sales for the Spanish fashion group, the world’s biggest clothing retailer and owner of Zara, Massimo Dutti, Bershka and Oysho.

Inditex generates more than half its sales in other currencies that have to be converted back into euros when it reports. Those currencies have strengthened slightly against the euro compared to a year ago, on average, helping reported sales. With the adverse foreign exchange effects removed, Inditex is under pressure to show it can deliver strong like-for-like sales without the margin dilution that has affected others. With less impact from foreign exchange, this will be an important year to prove the concept.

The apparel sector has been hit by out-of-season sales as savvy shoppers expect discounts and hunt for online bargains. Britain had its biggest fall in retail sales on record in May. Boohoo’s shares fell, despite the online British fashion retailer reporting robust sales, as lower margins disappointed investors.

Bangladesh makes it mandatory for buying houses to register with DoT

Buying houses in the garment and textile sector of Bangladesh have to get themselves registered with the Department of Textiles (DoT). Buying houses would have to file an application with the DoT with documents of an updated trade license, income tax certificate, a certificate of incorporation as a limited company, the estimated yearly turnover and a bank solvency certificate. The registration fee has to be paid through bank draft or pay order. The registrar will give the registration within 60 days of submitting the application and the validity of the registration certificate would be for three years. All buying houses with local and foreign investment and liaison offices of buyers and brands come under the rule.

The DoT is the sponsoring authority of all textile and clothing industries in Bangladesh. Many buying houses in Bangladesh run their business unregulated and there is no clear estimate of how many companies are working in the sector. There are some foreign buyers who work with the country’s readymade garment factories through their liaison offices and if they use any unfair means no action can be taken against them as they remain outside the purview of regulations. The idea is that bringing buying houses under registration would ensure accountability.

India's apparel grew lowest in five years, says study

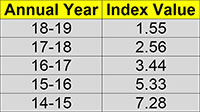

"As per CMAI's annual Apparel Index for FY2018-19, research conducted by DFU Publications on Indian apparel industry reveals, growth has been falling continuously for the past five years. In fact, except the first quarter of FY2018-19, the index values were much lower than comparable quarters in previous fiscal (FY2017-18). The Annual Index value of FY 2018-19 dipped to 1.71, the lowest ever in five years. Comparatively, the Annual Index in FY-2017-18 was 2.56; in FY-2016-17 it was 3.43 points similarly in FY-2015-16 it was 5.32 points and in FY-2014-15 it was 7.28 points."

As per CMAI's annual Apparel Index for FY2018-19, research conducted by DFU Publications on Indian apparel industry reveals, growth has been falling continuously for the past five years. In fact, except the first quarter of FY2018-19, the index values were much lower than comparable quarters in previous fiscal (FY2017-18). The Annual Index value of FY 2018-19 dipped to 1.71, the lowest ever in five years. Comparatively, the Annual Index in FY-2017-18 was 2.56; in FY-2016-17 it was 3.43 points similarly in FY-2015-16 it was 5.32 points and in FY-2014-15 it was 7.28 points. In fact, the index has been continuously falling over the years. FY2018-19 was marked by low business sentiment even during the festive season, perceived as the best time to make up for turnover losses, as buying is high at that time of year.

As per CMAI's annual Apparel Index for FY2018-19, research conducted by DFU Publications on Indian apparel industry reveals, growth has been falling continuously for the past five years. In fact, except the first quarter of FY2018-19, the index values were much lower than comparable quarters in previous fiscal (FY2017-18). The Annual Index value of FY 2018-19 dipped to 1.71, the lowest ever in five years. Comparatively, the Annual Index in FY-2017-18 was 2.56; in FY-2016-17 it was 3.43 points similarly in FY-2015-16 it was 5.32 points and in FY-2014-15 it was 7.28 points. In fact, the index has been continuously falling over the years. FY2018-19 was marked by low business sentiment even during the festive season, perceived as the best time to make up for turnover losses, as buying is high at that time of year.

The onus for fall in the last three years could be attributed to demonetization and the implementation of GST which have disrupted market sentiment and overall growth and the market has not yet recovered from their effects.

Q4 index growth dips across brand groups

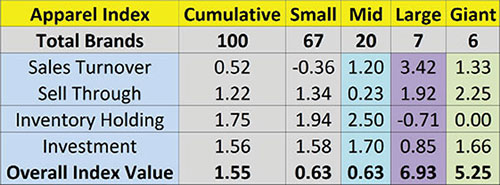

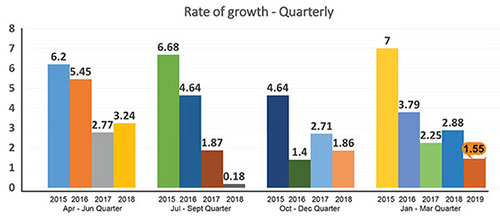

In the fourth quarter, CMAI's Apparel Index touched 1.55 points a clear reflection of low growth compared to previous quarter. In fact, Q4 (Jan-Mar FY 2018 -19) figures are lower than previous quarter’s 1.87. Like earlier, small brands sales dipped this quarter, and Giant brands at 5.25 points reported a drop in growth, compared to last quarter’s index figure of 6.00 and Q2s (July-Sept FY 2018 -19) impressive growth of 8.36. Except Large brands skyrocketing growth from 2.06 points in previous quarter to 6.93 points in Q4, all other brand groups reported a dip over last quarter.

previous quarter. In fact, Q4 (Jan-Mar FY 2018 -19) figures are lower than previous quarter’s 1.87. Like earlier, small brands sales dipped this quarter, and Giant brands at 5.25 points reported a drop in growth, compared to last quarter’s index figure of 6.00 and Q2s (July-Sept FY 2018 -19) impressive growth of 8.36. Except Large brands skyrocketing growth from 2.06 points in previous quarter to 6.93 points in Q4, all other brand groups reported a dip over last quarter.

CMAl's Q4 Apparel Index recorded a growth of 1.55 points, which is almost 2.5 times higher than the Index for Small brands (turnovers of Rs 10 to 25 crores) and Mid brands (turnover of Rs 25-100 crores) both at 0.63 points each. Large brands growth at 6.93 points, almost 4.5 times that of overall Index was the highest; at 5.25 points Giant brands’ growth is 3.38 times that of overall Index. In fact, this quarter it is the Large brands which recorded better growth. And, even though Giant brand’s rate of growth this quarter is much higher than others it is not as high as last quarter. At 1.55 points, overall Q4 index is lower than previous quarter’s Q3 Index at 1.86 points.

While Big brands (Mid, Large and Giant together) have grown at 6.08 points, much more than 3.52 points of previous quarter, individually Small and Mid brands dipped badly both to 0.63 from their previous quarter index values. Giant brands too have lost growth at 5.25 from 6.00 points previously. Only Large brands have pushed ahead to reach 6.93 (over three times) from their previous quarter’s 2.06 points.

Giant brands lost their highest growing group position to Large brands this quarter, however, both groups are still leading, outgrowing recessionary trends. Mid brands join Small brands this quarter failing to manage even moderate growth. Overall growth Index has been pulled down by these brand groups.

If Sales Turnover was to be considered as the only parameter for determining Apparel Index, this quarter then overall Index would have reflected a growth of 0.52 which is higher than previous quarter’s 0.88.

Sales Turnover down as Inventory Holding goes up

Cumulative Sales Turnover in Q4 is 0.52 a figure that is much lesser than that Q3’s 0.88. Around 39 per cent brands reported an increase in Sales Turnover this quarter compared to 48 per cent in previous quarter. “The decrease in sales turnover was mainly due to a slowdown in business due to a slowdown in the market post-Diwali. There was a substantial decrease in demand also,” explains Paresh Dedhia, Owner, Dare Jeans. On the contrary French menswear brand Celio reported positive sales turnover as Satyen Momaya, CEO, Celio points out, “The increase in sales turnover was due to our quality and we worked on an auto replenish model across our channels.” Similarly, lifestyle brand Monte Carlo gave a positive feedback as Mayank Jain, General Manager for the brand explained, “The reason for an increase in the sales turnover is we had a strong and good winter. Weather conditions were good and winter lasted for a longer period.” Adds Shitanshu Jhunjhunwala, Director, Turtle, “The increase in sales turnover was due to better work allocation. We had better sizes and availability of these sizes.”

brands reported an increase in Sales Turnover this quarter compared to 48 per cent in previous quarter. “The decrease in sales turnover was mainly due to a slowdown in business due to a slowdown in the market post-Diwali. There was a substantial decrease in demand also,” explains Paresh Dedhia, Owner, Dare Jeans. On the contrary French menswear brand Celio reported positive sales turnover as Satyen Momaya, CEO, Celio points out, “The increase in sales turnover was due to our quality and we worked on an auto replenish model across our channels.” Similarly, lifestyle brand Monte Carlo gave a positive feedback as Mayank Jain, General Manager for the brand explained, “The reason for an increase in the sales turnover is we had a strong and good winter. Weather conditions were good and winter lasted for a longer period.” Adds Shitanshu Jhunjhunwala, Director, Turtle, “The increase in sales turnover was due to better work allocation. We had better sizes and availability of these sizes.”

Almost 25 per cent brands reported a loss in Sales Turnover compared to 26 per cent in previous quarter. Except Large and Giant brands, other two groups this time reported sales losses. “The reason for the decrease in sales turnover was mainly due to closure of our stores,” observes Shyam, President 109° F.

Sell Through recorded an Index growth of 1.22 this quarter compared to 0.96 of previous quarter, still showing pressure on fresh good sales. Maximum growth in Sell Through was reported by Giant brands. Mid brands however, clocked in the lowest value of 0.23. As Shyam opines “The main reason for decrease in sell through is the online business has taken over a lot and has hampered business. It has actually killed it.”

Nearly 49 per cent brands reported an improvement in Sell Through, higher than 46 in Q3. “The major reason for an increase in sell through is the discounts given by brands before season and comparative price of the product. Imports from China is also a factor,” opines Rakesh Jain, CEO, Miss Grace.

Inventory Holding in Q4 is 1.75 points, this is higher than 1.6 points in Q3. Almost 61 per cent respondents across brands said their Inventory Holding moved north this quarter higher than 58 per cent in Q3, a very high number and they were responsible for pulling down overall apparel index value. Increase in Inventory Holding impacts overall index negatively. Higher Inventory Holding indicates more stocks in warehouses or shop shelves. Maximum increase in Inventory Holding was among Mid brands causing low index value; Giant brands on the other hand showed zero change in Inventory Holding. As Deepak Singhla, Marketing Head of Cantabil says “The decrease in inventory holding was because there was an increase in sale. Stock also sold off easily as well.” Agreeing on this point Jain says “Inventory holding decreased as store level sales have gone up, hence, there was no dead stock.”

However as per Momaya, “Inventory holding has actually not increased but has moved. There was more productivity and hence, inventory holding has gone down due to replenishment schemes.” However, Dedhia points out, “Increase in sales turnover and increase in inventory goes hand in hand. Payment cycles have stretched. There is less rotation of funds in the market.”

Investments, however, are low for the overall apparel segment, fresh Investments decreased to nearly 1.56 points, as against 1.62 points last quarter. Highest investments were done by Mid brands followed by Giant brands. Overall nearly 73 per cent respondents reported a rise in investments which is lower than 81 per cent in previous quarter. High investments in last quarter indicate most brands had to invest to manage albeit small growth which means growth is not coming easily.

An average outlook for next quarter

Around 58 per cent (last quarter 52 per cent) brands say the outlook for next quarter is ‘Average’. Generally, Q1 of the new fiscal, should be better as fresh summer sales picks up and prior to EOSS in July. However, there is no such excitement as the market has still not recovered from the earlier slowdown. Another factor could possibly be the Lok Sabh elections in Q2 this year which may have resulted in tepid response.

CMAl’s Apparel Index

CMAl’s Apparel Index aims to set a benchmark for the entire domestic apparel industry and helps brands in taking informed business decisions. For investors, industry players, stakeholders and policymakers the index is a useful tool offering concrete and credible information, and is an excellent source for assessing the performance of the industry. The Index is analysed on assessing the performance on four parameters: Sales Turnover, Sell Through (percentage of fresh stocks sold), number of days of Inventory Holding and Investments (signifying future confidence) in brand development and brand building.

The Apparel Index research is conducted by DFU Publications.

US/UK consumers expect brands to focus more on sustainability: Study

Consumers in the UK and the US want the fashion industry to become more sustainable. They now try to keep clothes longer because it’s better for the environment and are willing to pay more for sustainably-made versions of the same items, reveals a survey by e-commerce personalisation and retail AI platform Nosto. Consumers want retailers to clearly label clothes that are made in sustainable ways, offer discounts on clothing ranges that are more sustainable, do more to advertise and promote clothing that is made in sustainable ways, allow online shoppers to trade-in their used clothes for discounts on new items and automatically show people more sustainable alternatives to the items they are viewing online..

The survey reveals consumers also want fashion companies to reduce the amount of packaging, provide fair pay and good working conditions, use renewable and recyclable materials, make clothes that are designed to last longer and use fewer resources e.g. power, water, materials. But although brands are aware that consumers are increasingly concerned about sustainability in the fashion industry, they need to be more transparent and get better at communicating how they’re addressing it. The problem lies in knowing which fashion brands are really committed to sustainability. And consumers say it is difficult to know what fashion brands mean when they say they are committed to sustainability.

Sutlej Textiles expands capacity with new projects

Sutlej Textiles and Industries is expanding capacity through several new projects. The company is implementing a green fibre project to manufacture polyester staple fibre (PSF) by recycling of pet bottles at Baddi in Himachal Pradesh. The company has commenced work on the manufacturing of raw white & black recycled fibre with capacity of 120 MT/day. The total project cost is around Rs. 189 crores, and commercial production is expected to start in Q1 of FY20-21. The new plant will fulfill 75 per cent of Sutlej’s captive requirement of PSF, which is the key raw material.

Sutlej has also been continuously modernising its existing plant. The company invested around Rs 38 crores during FY19 towards technology upgradation and debottlenecking, etc. This will result in further improvement in efficiency and sustaining plant utilisation. Nearly 32 per cent of the spindleage and 67 per cent of the fabric weaving machines have been commissioned in the last decade, assuring high technological relevance.

To enhance its portfolio and presence in the home décor segment, Sutlej acquired American Silk Mills (ASM). The company is strengthening its product portfolio by leveraging the ASM design expertise and US presence, focussing on higher end markets in developed counties, building world-class design capabilities and improving product mix and broadening product portfolio.