![]()

FW

Currently valued at approximately $1.8 trillion, the global textile industry is undergoing a fundamental structural shift as the 2026 Heimtextil showcase highlights a move toward autonomous production ecosystem. Industry data suggests, AI integration in textile manufacturing is projected to grow at a CAGR of 28 per cent through 2030, driven by the need for hyper-localized supply chains and waste reduction. This shift is no longer merely conceptual; it is a commercial imperative for an industry facing heightened scrutiny over environmental impact and inventory volatility.

Algorithmic precision in manufacturing and procurement

The integration of generative design and predictive logistics is shortening the traditional eighteen-month fashion cycle into a lean, data-responsive framework. By utilizing AI-driven material visualizations, manufacturers are reporting a 30 per cent reduction in physical prototyping costs. As Tim Fu and other industry leaders noted during recent briefings, the convergence of algorithmic pricing and real-time demand sensing allows apparel brands to mitigate the risks of overproduction. This transition from mass production to ‘precision manufacturing’ ensures that textile output aligns strictly with verifiable market appetite.

Synthetic innovation and the new craft economy

A significant development in the 2026-27 cycle is the rise of ‘Digital Craftsmanship,’ where traditional weaving techniques are augmented by synthetic disruptions. Analysts observe, high-tech fibers and intelligent materials are increasingly capturing market share in the contract furnishing and hospitality sectors. The future of textiles lies in the intersection of biological sustainability and digital accuracy, notes an industry expert. As brands adopt these ‘glitch-aesthetic’ palettes and transformative materials, the sector is moving toward a circular economy model where every fiber is tracked via digital passports to ensure transparency and compliance.

As the premier global platform for home and contract textiles, Messe Frankfurt’s Texpertise Network connects over 50 design-driven trade fairs worldwide. Founded on a legacy of international trade mediation, the organization facilitates the primary exchange for high-performance fabrics, interior upholstery, and apparel components.

This feature is part of our dedicated series, "Wrap Up 2025 | Outlook 2026," investigating the structural shifts defining the next era of garment commerce.

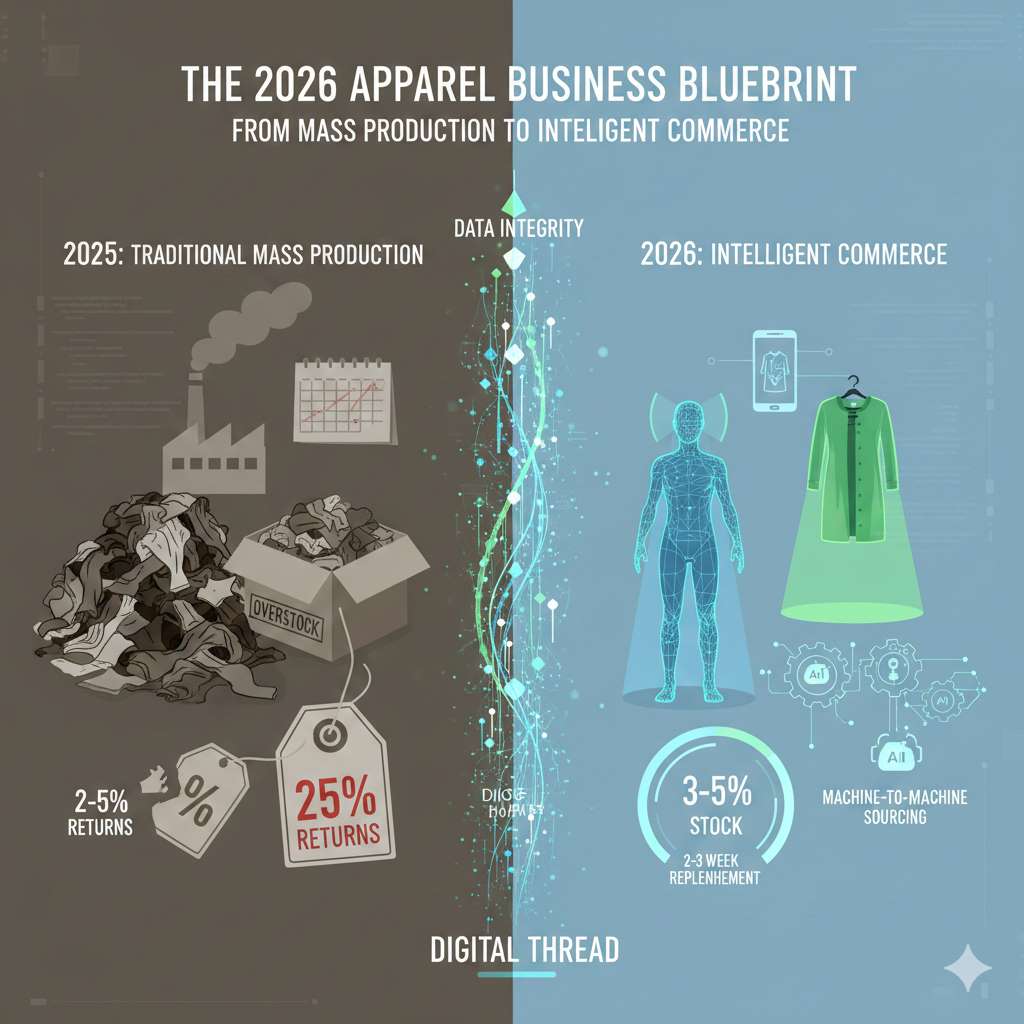

The transition from 2025 into 2026 marks the end of the "trial era" for digital tools in the textile world. For decades, the industry operated on guesswork, over-ordering, and massive end-of-season markdowns. As we enter 2026, the narrative has shifted toward a total integration of technology into the core business of making and selling clothes. We are moving away from traditional "Just-in-Time" manufacturing toward a model defined by Intelligent Commerce. This is a landscape where Artificial Intelligence is no longer a futuristic concept but the primary operating system for sourcing, planning, and manufacturing.

Fixing the Inventory Leak: The move to "Just-Tight-Enough" stock

The most significant financial drain on the apparel industry has always been the self-inflicted wound of over-production. In 2025, the standard practice for most retailers was to order 20% more stock than needed to buffer against shipping delays or sudden spikes in demand. This "Just-in-Case" mentality led to the $60 billion returns crisis and deep margin cuts. However, the 2026 "Inventory Manifesto" focuses on a shift toward Just-Tight-Enough stock levels.

By using AI to analyze real-time sales data and social trends, leaders are now adopting Micro-Batching. Instead of committing to massive production runs months in advance, brands are holding back 70% of their production capacity and only scaling the "winning" products in rapid 2-to-3-week replenishment cycles. This protects cash flow and ensures that capital is never locked in products that will eventually end up in a landfill.

Table 1: The New Economics of Inventory (2025 vs. 2026)

|

Performance Metric |

2025 Traditional Model |

2026 Intelligent Model |

|

Inventory Buffer |

15–20% (Over-stocking) |

3–5% (Precision Stock) |

|

Replenishment Speed |

8–12 Weeks |

2–3 Weeks |

|

Average Return Rate |

25% (Standard Sizing) |

8% (Made-for-Me Scaling) |

|

Deadstock Liquidation |

12% of Total Volume |

Under 4% of Total Volume |

Scaling Custom Clothes: The $65 bn "Made-for-Me" market

One of the most visible changes in 2026 is the industrialization of custom-fit clothing. In the past, "made-to-measure" was a slow, expensive service for luxury buyers. Today, technology has turned it into a $65 billion powerhouse. This shift is driven by the marriage of 3D body scanning and automated pattern-cutting. When a customer scans themselves using a smartphone, that data is sent directly to the factory floor.

The Industrialization of Fit: How 3D scanning and automated cutting scaled from "Made-to-Measure" to "Made-for-Me"

In the past, "made-to-measure" was a slow, manual process reserved for the luxury elite, requiring multiple in-person fittings and weeks of lead time. Today, 2026 has transformed custom apparel into a $65 billion powerhouse by moving personalization from the tailor’s table to the automated assembly line. This shift is driven by the marriage of 3D body scanning and automated pattern-cutting (APC).

The slow, error-prone tape measure has been replaced by smartphone LiDAR scans and in-store 3D booths that capture 100,000 data points in seconds. This digital avatar is then instantly synced with AI-driven pattern-making software. Instead of a human grader manually adjusting a "Size Large" template (the old "Made-to-Measure" way), the AI generates a unique, one-off cutting marker designed specifically for the customer's unique proportions—a true "Made-for-Me" model. This marker is sent directly to laser-cutting machines that slice fabric with sub-millimeter precision. By industrializing what was once a craft, factories in global hubs can now process "lot-size-one" orders with the speed of mass production, finally solving the $60 billion returns crisis by ensuring the garment fits perfectly before the first cut is even made.

The New Way of Buying and Sourcing, Agentic Commerce: When machines talk to factories

The B2B sourcing landscape is undergoing a radical change as we move into 2026. The traditional method of "relationship-based" sourcing—where buyers and suppliers spent months negotiating over catalogs—is being replaced by Agentic Commerce. Major retailers like Zara and Walmart are now deploying AI Agents that act as autonomous buyers. These digital agents "talk" directly to factory ERP systems to check fabric availability, machine capacity, and even real-time shipping costs.

In this new environment, if a supplier's digital system cannot communicate via high-speed APIs, that supplier becomes invisible to the world’s largest buyers. The industry is moving from "who you know" to "how clean is your data." This shift is so profound that legal experts expect 2026 to see the first landmark "AI-sues-Supplier" lawsuit, likely centered on a factory feeding misleading capacity or sustainability data into a retailer's autonomous procurement system.

Table 2: The 2026 Apparel Tech Pulse – Sectoral growth & operational data

|

Sector / Technology |

2025 Adoption Level |

2026 Market Impact |

Primary Value Driver |

|

|

Custom Apparel (POD) |

$48 Billion |

$65 Billion |

Scalable Personalization & Zero Deadstock |

|

|

AI in Fashion (Overall) |

$2.92 Billion |

$3.99 Billion |

40% CAGR; Design to Retail Integration |

|

|

Technical Embroidery |

12% Adoption |

42% Growth |

Smart Fabrics & Integrated Biometrics |

|

|

Machine-to-Machine (M2M) |

Experimental |

20% of B2B Quotes |

Automated Procurement & Replenishment |

|

|

Active Governance (GRC) |

Compliance-led |

Board-level Risk |

Real-time Supply Chain Ethical Audits |

|

Active Governance: Managing risk in Real-Time

Geopolitical instability and supply chain ethics have become the top risks for apparel boards in 2026. The old model of "passive governance", waiting for a yearly audit report to see if a factory is compliant, is no longer enough. The industry has moved to Active Governance, where digital agents monitor every tier of the supply chain in real-time.

These AI-augmented systems track everything from a factory’s carbon footprint to labor law compliance and local political disruptions. This allows companies to build Operational Resilience by automatically rerouting orders or switching suppliers the moment a risk is detected. For the C-Suite, this means moving away from "managing crises" to "preventing disruptions" through a live, digital view of the entire global network.

C-Suite Outlook: The CEO’s strategy for an autonomous era

As we look toward the rest of 2026, the leadership mandate for the apparel industry is clear: the focus must be on Digital Infrastructure. Strategic leaders are no longer just buying machines; they are investing in the "Integrity of the Thread," which now refers to the data that follows a garment from the cotton field to the consumer's closet.

C-Suite priorities have shifted toward ensuring that all company systems, from design to logistics, are fully interoperable. This requires a massive effort in reskilling the workforce, moving employees away from manual tasks like order chasing and toward managing the AI systems that handle the heavy lifting. The goal for 2026 is to create a business that is "data-fluid," where information moves faster than the fabric itself. This reallocation of capital toward Agentic Commerce is creating a massive market impact, as seen in the jump from experimental M2M pilots to a world where 20% of B2B quotes are generated and processed entirely by machines.

Editor’s Conclusion: The integrity of the ‘Digital Thread’

The takeaway for 2026 is that the apparel business is no longer just about fashion; it is about the precision of information. The "Wrap Up of 2025" has shown us that the old ways of mass-producing and hoping for sales are leading to financial ruin. The "Outlook for 2026" offers a much brighter path for those who embrace Intelligent Commerce.

By using AI to eliminate inventory waste, scaling "Made-for-Me" production to end the returns crisis, and adopting "Active Governance" to protect brand reputation, the industry is becoming leaner and more profitable. However, this progress depends entirely on Data Integrity. In a world where machines are doing the buying and factories are running on autonomous schedules, a single piece of bad data can be more costly than a thousand yards of wasted silk. The digital thread is now the most important part of the garment.

Vietnam’s textile and apparel (T&A) exports to Canada are projected to surpass $1.3 billion in 2025, marking a robust 10 per cent Y-o-Y growth. This growth is underpinned by a structural shift toward ‘closed-loop’ production models that satisfy the strict ‘yarn-forward’ rules of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). By securing raw materials from member states - including cotton from Brazil and Australia - Vietnamese manufacturers are successfully neutralizing the 17–18 per cent import duties that previously hindered competitiveness, effectively doubling export value since 2018.

Industrial expansion and direct partnership models

To capitalize on this trajectory, major players like Viet Hong Textile Dyeing JSC are aggressively scaling operations. The firm is expanding its denim production capacity from 1.2 million to 2 million meters per month to meet North American demand. Simultaneously, Bao Minh Textile JSC is leveraging its fully integrated manufacturing chain to penetrate the high-end woven fabric segment. Industry leaders are now moving beyond the traditional OEM model, seeking direct partnerships with Canadian retailers to eliminate third-party branding costs and deepen vertical integration within the global value chain.

Infrastructure hubs and regional logistics

The sector’s growth is further bolstered by Canadian capital flowing into Vietnamese manufacturing hubs. Investors are increasingly utilizing Vietnam as a strategic distribution base for the Asia-Pacific region, rather than just a low-cost sourcing site. Despite logistical hurdles and rising transportation costs, the recognized compliance and high technical standards of Vietnamese facilities have solidified the nation's position as a reliable, high-margin partner in a diversifying global supply ecosystem.

Vietnam’s textile sector specializes in high-standard denim, yarn, and woven fabrics, primarily serving North American and EU markets. Growth plans center on maximizing CPTPP tariff exemptions through domestic material sourcing and technological upgrades. With 2026 export targets aiming for a 12 per ecnt increase, the industry is transitioning from a commodity supplier to a sustainable, high-value global manufacturing hub.

In a high-level consultation held on January 5, 2026, Kamel Al0-Wazir, Deputy Prime Minister for Industrial Development, Egypt unveiled a series of measures aimed at localizing the entire textile value chain. The initiative seeks to bridge supply-chain gaps in the ready-made garments (RMG) and home furnishings sectors, which currently face an over-reliance on imported fabrics. By mandating that new garment factory licenses include spinning and textile manufacturing components, the Industrial Development Authority (IDA) is enforcing a policy of full industrial integration to ensure ‘sovereign’ production cycles.

Combating customs evasion and market irregularities

A newly formed committee, comprising the Ministry of Industry and the Federation of Egyptian Industries, has been tasked with curbing customs evasion and ‘predatory’ pricing from unregulated imports. Al-Wazir announced, the committee will intensify monitoring of factories in free zones and those utilizing ‘temporarily admitted’ raw materials. The objective is to ensure that imports are strictly calibrated to actual production capacities, protecting local manufacturers who adhere to stringent quality standards from unfair competition.

Partnerships and petrochemical independence

The government is aggressively pursuing private-sector partnerships to modernize state-owned spinning and weaving mills. These joint financing models allow private entities to leverage public-sector infrastructure - including land and machinery - while providing operational expertise. Furthermore, to reduce dependence on imported polyester, the Ministry is scaling up investment in the petrochemical sector, targeting a significant increase in domestic yarn production of cotton, flax, polyester, and wool to meet the rising demand from global brands sourcing in Egypt.

Egypt’s textile sector is a cornerstone of the national economy, employing approximately 1.5 million workers and targeting $12 billion in exports by 2031. The government’s Vision 2030 strategy focuses on revitalizing state-owned factories through $1.5 billion in upgrades and establishing integrated ‘Textile Cities’ in Minya and Fayoum. Key product categories include high-quality Giza cotton, flax, and RMG for the US and EU markets, with growth driven by strategic petrochemical localization and competitive energy costs.

The high-stakes consolidation of European luxury has entered a definitive new phase as the Prada Group officially completed its $1.375 billion acquisition of Versace from Capri Holdings in December 2025. This transaction effectively reverses the 2018 blockbuster deal where the American conglomerate, then known as Michael Kors Holdings, purchased the storied Italian maison for $2.1 billion. By returning the brand to its domestic roots, Prada Group is signaling a shift away from the ‘accessible luxury’ volume model toward a strategy of disciplined exclusivity. The acquisition follows the collapse of a proposed $8.5 billion merger between Tapestry and Capri Holdings, which was blocked by US regulators, leaving Capri to divest its ‘family silver’ to stabilize its balance sheet.

Financial reset and operational synergiets

With revenues rising by 15 per cent in 2024, Prada Group is leveraging its robust retail momentum to integrate Versace into its high-performance distribution network. For Capri Holdings, the sale serves as a critical deleveraging event, enabling the repayment of substantial debt following a fiscal year where Versace revenue dipped by 21 per cent. This acquisition provides Versace with a strong platform rooted in Italian craftsmanship, states Patrizio Bertelli, Chairman, Prada Group. The transition occurs as the personal luxury goods market is projected to reach $301 billion by 2026, driven by a 4.2 per cent compound annual growth rate.

Pioneering a phygital luxury future

Under new ownership, Versace is set to accelerate its digital transformation by integrating AI-driven personalized shopping and ‘Digital Product Passports’ to meet 2026 transparency mandates. By combining Miuccia Prada’s organizational rigor with Donatella Versace’s high-octane aesthetic, the group aims to capture the ‘Silver Spender’ demographic while simultaneously pivoting toward Gen Z consumers, who are expected to constitute 75 per cent of luxury buyers by the end of 2026. This strategic realignment prioritizes scarcity and heritage over mass-market penetration, marking a significant evolution in the global apparel landscape.

Prada Group is a dominant Italian luxury powerhouse managing iconic brands including Prada, Miu Miu, and Church’s. It specializes in high-end leather goods, ready-to-wear apparel, and footwear, primarily targeting affluent consumers in the Asia-Pacific, European, and North American markets.

The Ministry of Electronics and Information Technology (MeitY) has accelerated the deployment of ‘AI Kosh’, a centralized national library designed to consolidate non-personal datasets for large language model (LLM) training. As of early 2026, the platform has scaled to host over 5,500 curated datasets and 251 pre-trained models, effectively addressing the ‘data poverty’ that previously hindered domestic AI development. By providing access to high-fidelity metadata from sectors like agriculture, healthcare, and 12 Indic languages via the Bhashini division, the government aims to facilitate the creation of indigenous foundational models that are culturally and linguistically nuanced.

Strategic infrastructure and economic projection

To complement the data repository, the IndiaAI Mission has expanded its compute capacity to 38,000 GPUs, offering them to researchers and startups at a subsidized rate of approximately Rs 65 per hour. This integrated approach is vital for the 22 Indian firms currently developing LLMs, including BharatGen and Sarvam AI. Sovereign AI isn't just about software; it's about owning the data-to-compute pipeline, noted a senior MeitY official. With the AI sector projected to contribute nearly $500 billion to India’s GDP by 2027, the success of AI Kosh is viewed as a prerequisite for achieving global leadership in the ‘AI for All’ initiative.

Overcoming data poisoning and governance hurdles

Despite the infrastructure gains, the project faces critical challenges regarding data integrity and cybersecurity. Experts warn of ‘model poisoning’ risks, where manipulated inputs could degrade the accuracy of public LLMs. Furthermore, while the Digital Personal Data Protection (DPDP) Act 2023 provides a legal framework, the technical implementation of ‘machine unlearning’- the ability to remove specific data points from a trained model - remains a complex hurdle for developers using these public datasets to build commercial-grade applications.

MeitY serves as the primary architect of India’s Digital Public Infrastructure, managing large-scale platforms like Aadhaar, UPI, and now AI Kosh. The ministry focuses on democratizing technology through open-source stacks and sovereign data repositories. Current growth plans involve scaling AI compute portals to 50,000 GPUs by 2027 to support a $1 trillion digital economy.

Starting 6 January 2026, Asos is deploying a pioneering ‘returns transparency’ dashboard within its UK mobile application, marking a decisive shift from punitive fees to behavioral data sharing. This initiative allows shoppers to view their real-time return percentages, a move designed to curb the ‘serial returner’ phenomenon that currently costs the UK e-commerce sector an estimated £27 billion annually. Under the refreshed framework, customers maintaining a return rate above 70 per cent will incur a $5.02 fee on orders where the retained value falls below US $50.80. For those exceeding an 80 per cent threshold, an additional $5.02 restocking fee applies, reflecting the mounting logistics pressure on digital-first retailers.

Bridging the profitability gap

The rollout follows a period of aggressive financial restructuring. Despite a 15 per cent decline in group revenue to £2.5 billion for the fiscal year ending August 2025, ASOS successfully narrowed its pre-tax losses by nearly £100 million. By focusing on ‘high-quality’ sales -transactions with a lower probability of reversal - the retailer increased its profit per order by approximately 30 per cent Y-o-Y. Sustainability in e-commerce requires a reset of the unit economics, states Ben Blake, Executive Vice President - Customer and Commercial. Transparency empowers the majority of our fair-use shoppers while protecting the business from unsustainable reverse-logistics cycles.’

Mitigating the sizing crisis

To facilitate this transition without alienating its core Gen Z demographic, ASOS is integrating 360-degree product videos and AI-driven virtual fit assistants. These tools aim to address the root cause of returns, as industry data reveals that 81 per cent of shoppers still prioritize free returns when selecting a merchant. By gamifying ‘good’ shopping behavior and issuing threshold alerts before fees are triggered, Asos is attempting to balance the fiscal necessity of stricter policies with the personalized experience demanded by the modern fashion consumer.

A global online fashion destination targeting 18-to-34-year-olds, Asos offers over 850 partner brands alongside its dominant own-brand labels, including Asos Design and the Topshop/Topman joint venture, primarily serving the UK, US, and European markets.

The 2026 ‘Brand Relaunch’ focuses on expanding gross margins to 50 per cent through full-price sales and inventory reduction. After cutting stock levels by 60 per cent since 2022, the company projects an adjusted EBITDA of up to £180 million for FY26.

This report is the eighth installment of the "Wrap Up 2025, Outlook 2026" series, providing a definitive roadmap for the industry’s high-growth categories and regional shifts.

The 2026 global textile landscape is defined by a decisive move away from general-purpose manufacturing toward specialized, high-performance materials. As we move through the year, capital expenditure in the industry is being redirected into the "Double Agenda", fabrics that meet stringent performance requirements while remaining fully compliant with new global trade mandates. The total global textile market is valued at approximately $2,281.51 billion for 2026, maintaining a compound annual growth rate (CAGR) of 7.35%. This growth is increasingly concentrated in segments that offer measurable functional value over basic aesthetics.

2026 sector performance and growth projections

The following data outlines the market valuation and growth trajectories for the dominant industry segments as they stand in the current 2025–2026 cycle.

|

Sector/Segment |

2025 Market Size (Est) |

2026 Projected Size |

CAGR (2025-26) |

Key Growth Catalyst |

|

Apparel (Overall) |

$1.84 Trillion |

$1.91 Trillion |

3.80% |

Casualization & E-commerce |

|

Performance Textiles |

$105.40 Billion |

$113.72 Billion |

7.90% |

Biometric & Smart Sensing |

|

Knits & Sportswear |

$325.40 Billion |

$348.18 Billion |

7.00% |

Tech-Performance Blends |

|

Technical Textiles |

$255.12 Billion |

$271.83 Billion |

6.55% |

Med-Tech & Mobil-Tech |

|

Home Textiles |

$149.09 Billion |

$158.16 Billion |

6.08% |

Smart Bedding & Wellness |

|

Denim Apparel |

$78.90 Billion |

$84.11 Billion |

6.61% |

Waterless Dyeing & Circularity |

|

Bedroom Linen |

$67.09 Billion |

$71.16 Billion |

6.07% |

Functional Finishes |

Segment Analysis: Commercial dynamics and strategic stories

Performance Textiles: The "Sensing & Adaptive" suite

Performance textiles have emerged as the fastest-growing niche, projected to reach $113.72 billion in 2026 with an industry-leading 7.9% CAGR. This segment has evolved from simple moisture-wicking gear into "Adaptive Wear", fabrics that use conductive yarns and chromic materials to react to body temperature or environmental shifts. Commercial adoption is being driven by the integration of biometric sensors directly into the fiber matrix, allowing garments to track heart rate and muscle fatigue without external devices. In 2026, the market has split into two distinct tiers: high-end professional "Bio-data" wear and mass-market "Climate-adaptive" apparel that provides breathable insulation in cold weather and active cooling in heat. This segment is a primary winner for North American and Japanese firms, who hold the majority of patents for conductive textile polymers.

Home Textiles: The "Functional Wellness" suite

The home textile sector has transitioned from a decorative category into a health-focused "Functional Wellness" suite. Currently valued at $158.16 billion, the market is being driven by the "Bedroom Linen" sub-segment, which holds a commanding 45% share of the total home textile category. Commercial interest has moved beyond thread counts to "Smart Bedding", fabrics treated with phase-change materials for temperature regulation and silver-ion coatings for antimicrobial protection. These functional finishes are the primary engine behind the 6.08% CAGR, as consumers increasingly view their bedding as a tool for sleep hygiene. From a trade perspective, India has solidified its position as a global leader in this space by combining its massive organic cotton reserves with proprietary technical finishes to satisfy high-end retail demand in the US and EU.

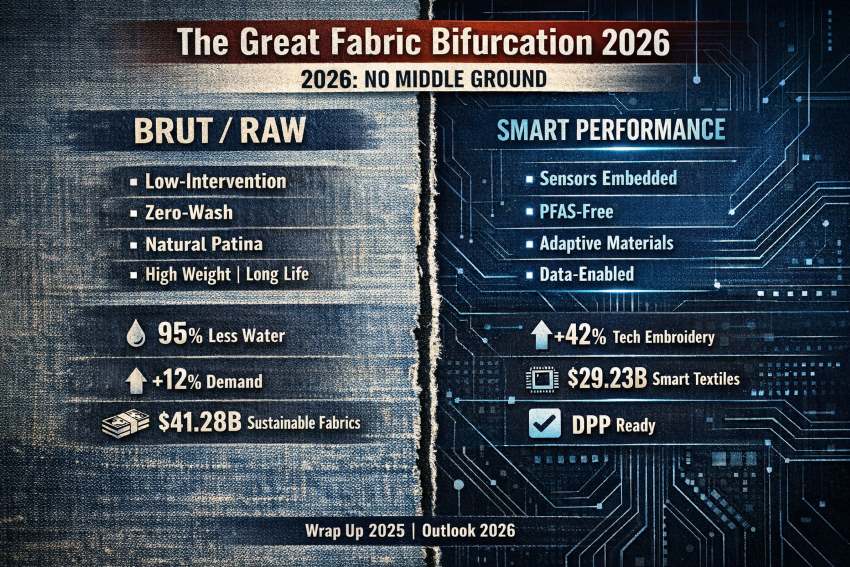

Denim: From advocacy to "Invisible Circularity"

Denim has moved past the era of sustainability "pledges" into an era of rigorous engineering known as "Invisible Circularity." The segment is projected to reach $84.11 billion this year, with a 6.61% CAGR. The commercial goal for 2026 is the production of jeans that maintain a premium, heritage look but are designed for 100% recyclability. Nearly 40% of global manufacturers have now integrated waterless dyeing and laser-finishing technologies to remain compliant with tightening environmental standards in major import markets. The rise of mono-material denim, where even the stitching and hardware are made from shreddable, recyclable polymers;is the current benchmark for market entry. Turkey and India remain the dominant exporters in this high-tech denim race, while Mexico is securing a larger share of the US market through near-shore logistical advantages.

Knits & Sportswear: The "Bio-Performance" frontier

Knits and sportswear represent one of the fastest-growing categories, with a projected size of $348.18 billion and a 7.0% CAGR. The story here is the replacement of petroleum-based polyesters with bio-based synthetics derived from algae and corn. This shift is not just environmental but functional, as these new fibers offer superior moisture-wicking and cooling properties. The adoption of 3D Seamless Knitting has become the industry standard for high-performance brands, as it reduces fabric waste by roughly 30% and significantly lowers labor costs. Vietnam and Bangladesh are the primary winners in this segment, having aggressively upgraded their factory floors with automated knitting systems to capture volume from global athletic giants.

Technical Textiles: The "Industrial Backbone"

Technical textiles are the most resilient pillar of the industry, projected to reach $271.83 billion in 2026. This segment is no longer a niche but an essential industrial component. Growth is heavily concentrated in Med-Tech (implantable textiles and surgical non-wovens) and Mobil-Tech (lightweight, reinforced fabrics for electric vehicle interiors). This is a high-margin sector where intellectual property and patents dictate market power. Consequently, the USA, Japan, and Germany remain the dominant exporters of specialized technical fibers, while China focuses on the high-volume production of industrial filtration and protective gear.

Global Trade Matrix: Winners & Losers (2026 Forecast)

The global trade landscape is being reshaped by regional capabilities in technology and regulatory compliance. Countries that have invested in "green" infrastructure are seeing an influx of foreign direct investment, while those relying on low-cost, high-pollution models are seeing a contraction in orders.

|

Segment |

Regional Winners (Growth) |

Regional Losers (Stagnation) |

Primary Commercial Factor |

|

Performance Textiles |

USA, Japan, South Korea |

China (Standard Synth.) |

Biometric Patent Control & Smart Tech |

|

Home Textiles |

India, Turkey |

China (Volume), Pakistan |

Wellness certifications & Traceability |

|

Denim |

Vietnam, Mexico, Turkey |

USA (Manufacturing), Lesotho |

Near-shore logistics & Waterless tech |

|

Knits/Sportswear |

Bangladesh, Vietnam |

Italy (Mid-tier), Cambodia |

3D-Knitting & ESG Compliance |

|

Technical Textiles |

USA, Japan, Germany |

Rest of Asia (Low-end) |

IP Patents & MedTech Innovation |

Major Exporters and Importers: Leading Dynamics

● India: A major winner in 2026 due to the Production Linked Incentive (PLI) scheme, which has moved the country's export profile from raw cotton to high-value technical textiles and functional home linens.

● China: While remaining the world’s largest exporter by volume, China is losing market share in basic apparel as it moves its manufacturing base toward high-value synthetic fibers and AI-integrated textile machinery.

● Vietnam & Bangladesh: These nations have successfully transitioned from basic cut-and-sew operations to sophisticated, tech-enabled hubs for sportswear and high-end knits, benefiting from strategic free trade agreements.

● USA & EU: As the primary importers, these regions are the "gatekeepers" of the 2026 market. Their demand for supply chain transparency (via the Digital Product Passport) is forcing global exporters to adopt expensive but necessary traceability technologies.

Losers: Countries like Pakistan are facing commercial headwinds due to rising energy costs and a lack of investment in high-tech finishing, while Lesotho and Cambodia are seeing a decline in orders as brands prioritize "Green-ready" hubs that can guarantee lower carbon footprints.

As the fashion industry confronts a staggering 92 million tons of annual waste, the textile recycling sector has transitioned from a niche sustainability effort into a critical commercial pillar. The global market is valued at $6.34 billion in 2025, with projections reaching $9.94 billion by 2033. This growth is increasingly fueled by Extended Producer Responsibility (EPR) mandates across Europe and the US, which effectively end the era of ‘disposable’ inventory by holding brands financially accountable for a garment's entire lifecycle.

The chemical advantage and AI integration

Traditional mechanical recycling, which often degrades fiber length, is being challenged by high-precision chemical processes. Chemical recycling now dominates the sector with a 52.14 per cent market share, enabling the regeneration of polyester and blended fabrics into ‘virgin-quality’ fibers. This technological shift is augmented by AI-powered sorting systems, which have demonstrated the ability to reduce contamination rates by up to 45 per cent. By utilizing near-infrared (NIR) sensors and machine learning, facilities can now identify 13+ fiber types at speeds exceeding one garment per second, solving the long-standing bottleneck of manual labor.

The US market and regulatory tailwinds

The US segment is experiencing an accelerated 7.96 per cent CAGR, significantly outpacing global averages as domestic brands secure consistent feedstock for recycled polyester lines. However, the industry faces a sharp divide: while 70 per cent of consumers demand sustainable fabrics, only 1 per cent of textiles are currently recycled back into new garments. To bridge this ‘circularity gap,’ major retailers are integrating digital product passports to enhance traceability. As landfill bans tighten, the transition toward a closed-loop system is no longer a branding choice but a necessary hedge against rising waste-dispochemical depolymerization sal premiums and regulatory fines.

Circular infrastructure and market outlook

Textile recyclers manage the collection and reprocessing of post-consumer and industrial waste into high-value raw materials. Key markets include North America and Asia-Pacific, with growth focused on chemical depolymerization for polyester. Historically a fragmented sector, it is now scaling through brand partnerships to meet 2030 zero-waste targets.

The Government of India has officially extended the application window for the Production Linked Incentive (PLI) Scheme for Textiles until March 31, 2026. This strategic extension, announced by the Ministry of Textiles on January 2, 2026, aims to capitalize on heightened investor interest in high-growth segments such as Man-Made Fiber (MMF) apparel and technical textiles. By providing an additional quarter for fresh proposals, the government seeks to broaden the industrial base beyond traditional cotton, aligning with the ambitious national target of achieving US$ 100 billion in textile exports by 2030.

Facilitating inclusion and scale

Recent amendments have significantly lowered the barrier to entry, reducing minimum investment thresholds to Rs 50 crore for smaller units and Rs 150 crore for larger projects. These adjustments have already yielded substantial results; as of late 2025, 91 companies have been selected, committing an aggregate investment of Rs 7,731 crore. This fiscal push is designed to move Indian apparel manufacturing toward a vertically integrated model, enhancing cost-competitiveness against global rivals like Vietnam and Bangladesh. The Ministry reports, the scheme has already generated over 30,000 jobs, with turnover figures exceeding Rs 7,200 crore.

Strategic alignment with global standards

The extension arrives as the industry prepares for the National Textiles Ministers’ Conference later this month in Guwahati. Beyond domestic scaling, the PLI framework is being synchronized with global ESG (Environmental, Social, and Governance) mandates. By incentivizing technical textiles - used in healthcare, defense, and automotive sectors - India is diversifying its export basket to mitigate the risks associated with volatile cotton cycles. The revised norms ensure that even mid-sized manufacturers can now integrate into the global value chain, stated a Ministry official, highlighting that the move is essential for leveraging recent Free Trade Agreements (FTAs) with the UK and Australia.

Textile PLI initiative

The Production Linked Incentive (PLI) Scheme for Textiles focuses on promoting MMF apparel, MMF fabrics, and technical textiles. With a total outlay of Rs 10,683 crore, the initiative targets large-scale manufacturing and export growth. Launched in 2021, it aims to transform India into a global textile hub by 2030.