FW

Lenzing reinforces governance stability with key leadership reappointments

The Lenzing Group has prioritized institutional stability following its 82nd Annual General Meeting on April 23, 2026, by securing the long-term mandates of its primary oversight body. Shareholders moved to re-elect Dr Astrid Skala-Kuhmann, Mag Gerhard Schwartz, and Mag Helmut Bernkopf to the Supervisory Board, extending their terms until the end of FY30-end. This strategic move ensures that the specialty fiber producer maintains a consistent leadership trajectory as it navigates the transition from a linear to a circular economy. By retaining experienced directors, the group aims to provide a steady hand for its science-based climate action plan, which targets a significant reduction in greenhouse gas emissions over the same period.

Leadership structure solidified for upcoming fiscal cycles

In a subsequent constitutive session, the board solidified its executive oversight by re-electing Patrick Lackenbucher as Chairman. This structural continuity is bolstered by the appointment of Carlos de Almeida and Stefan Fida as deputy chairmen, overseeing a ten-member board elected by shareholders and supplemented by five delegates from the Works Council. Beyond personnel changes, the assembly formally discharged the Managing and Supervisory boards for the 2025 financial year, which saw the company generate €2.60 billion in revenue. To maintain transparency standards, KPMG Austria was appointed as the auditor for the FY26, with a specific mandate to oversee consolidated sustainability reporting—a critical function for a firm currently managing an annual fiber capacity of over 1.1 million tonnes.

Aldo strategic SS26 launch targets high-growth footwear segments

Aldo has formally debuted its Spring-Summer 2026 collection, a strategic launch aimed at capturing the burgeoning demand for ‘comfort-led statement’ footwear. Moving beyond purely aesthetic cycles, the brand has integrated its proprietary Pillow Walk technology across 40 per cent of the new range, addressing a critical shift in consumer behavior where ergonomic support is now non-negotiable in fashion-forward categories. Market analysts observe, this technical integration allows Aldo to maintain its premium pricing power in a competitive global retail landscape, where the footwear sector is projected to reach $430 billion by late 2026, driven largely by hybrid lifestyle needs.

Navigating supply chain dynamics through technical diversification

The SS26 rollout highlights a significant shift toward high-performance synthetic materials and low-impact dyeing processes, mitigating the impact of rising leather costs and energy-intensive manufacturing. This collection serves as a primary case study for Aldo’s 2026 sustainability roadmap, which prioritizes circular design without compromising the high-shine finishes and architectural heels demanded by urban professionals. Versatility is the primary driver for our current demographic, noted a senior regional director. By consolidating seasonal trends with sustainable sourcing, Aldo is effectively future-proofing its margin stability against the 12% fluctuation currently seen in global raw material indices.

Retail expansion and the digital fulfillment synergy

To maximize market penetration, Aldo is leveraging an omnichannel distribution model that pairs physical experience centers with AI-driven inventory replenishment. In key expansion zones like India and Southeast Asia, the brand is capitalizing on a 15 per cent Y-o-Y growth in the premium footwear segment. By utilizing real-time consumer data to influence local assortments, Aldo is bypassing traditional inventory bottlenecks, ensuring that high-demand silhouettes—such as modular sandals and statement pumps - remain accessible across both metropolitan storefronts and high-speed D2C digital platforms.

Founded in 1972 in Montreal, ALDO is a global leader in fashion footwear and accessories, operating in over 100 countries. The group specializes in trendy, accessible luxury for men and women. Its 2026 growth focuses on ergonomic technology and digital-first retail, aiming for consistent high-single-digit revenue growth through sustainable infrastructure.

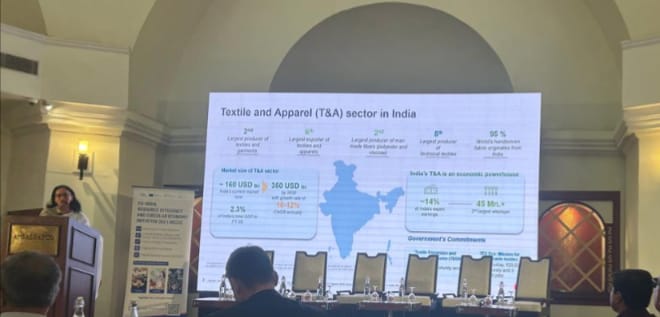

CITI advocates for National Fiber Mission to boost Indian textile value chain

The Confederation of Indian Textile Industry (CITI) has formally called for a comprehensive harmonization of India’s ‘fiber-to-fabric’ ecosystem through the newly proposed National Fiber Scheme. This strategic appeal aims to bridge the productivity gap between raw material output and finished apparel exports. As of April 2026, sector data indicates a 2.21 per cent decline in cumulative textile and apparel exports, a trend CITI believes can be reversed by integrating spinning and weaving more tightly into national incentive missions.

Mitigating supply shocks through raw material security

Current industry bottlenecks, including a 50 per cent effective tariff burden in the US market, have highlighted the vulnerability of fragmented supply chains. Ashwin Chandran, Chairman, CITI, notes, competitiveness begins with raw material security. To counter rising overheads and a 14 per cent Y-o-Y degrowth in March exports, the industry is advocating for a Cotton Price Stabilisation Fund and duty-free access to specialized Extra Long Staple (ELS) fibers. These measures are designed to ensure that Indian manufacturers can offer competitive pricing despite global economic headwinds and energy constraints.

Leveraging hub-and-spoke clusters for global integration

The sector’s growth plan centers on the rollout of PM-MITRA mega parks, which are transitioning from planning to execution phases in 2026. These parks serve as a case study for localized integration, aiming to reduce logistics costs - which currently inflate Indian export prices - by housing the entire value chain in one perimeter. By aligning these hubs with blockchain-based traceability and the EU’s Digital Product Passport mandates, CITI expects to capture a larger portion of the $263 billion premium fiber market, moving India closer to its ambitious $350 billion industry target by 2030.

Leading national chamber

The Confederation of Indian Textile Industry (CITI) is the leading national chamber representing the entire textile value chain. It services domestic and international markets, primarily focusing on cotton and man-made fibers. CITI is currently driving a modernization roadmap centered on ESG compliance and technical textiles to restore export momentum and stabilize long-term financial performance.

Hams Group strengthens market leadership with top tier supplier recognition

In a decisive move that underscores the shifting dynamics of the Bangladeshi apparel sector, Hams Group has secured the Gold Award at the Next Sourcing Bangladesh Awards 2025. This recognition serves as a testament to the organization’s operational excellence during a period of significant global trade recalibration. Unlike the volume-heavy strategies of the past, Hams Group has distinguished itself by leveraging a fully vertical manufacturing model - integrating spinning, knitting, and dyeing - to mitigate the supply chain volatility currently impacting the broader South Asian textile landscape.

Strategic resilience amid global economic headwinds

The award arrives as the industry navigates a complex 2026 fiscal environment, characterized by an 18 per cent fluctuation in knitwear export values and rising overhead costs linked to regional energy constraints. While many manufacturers face contraction, Hams Group has maintained a robust delivery schedule for global partners like Next, Primark, and H&M. Reliability is the new currency in fashion sourcing, stated a senior procurement executive at Next Sourcing. Hams Group has demonstrated an atypical ability to maintain lead times through internal resource management and advanced automation, setting a precedent for the post-LDC graduation era.

Future-proofing through de-carbonization and circularity

Central to the group’s recent success is its investment in LEED-certified infrastructure and water-efficient processing. As the European Union’s Digital Product Passport (DPP) regulations loom for late 2026, HAMS has already integrated blockchain-based traceability across its knitwear lines. By reducing fabric wastage to under 3 per cent via AI-driven cutting systems, the company is not only optimizing its cost structure but also aligning with the stringent ESG mandates of its Tier-I European clientele. This proactive stance on circularity positions the group to capture a larger share of the value-added segment as buyers transition away from high-carbon production hubs.

A premier vertically integrated apparel manufacturer, Hams Group specializes in high-performance knitwear and complex garments. Operating from a state-of-the-art manufacturing base in Bangladesh, the company serves major retail conglomerates across Europe and North America. With a 2026 growth strategy focused on technical textiles and synthetic fiber diversification, Hams continues to deliver consistent financial performance, underpinned by its commitment to carbon neutrality and Industry 4.0 automation.

STCH highlights deep-tech integration in apparel supply chain with new funding round

Bengaluru-based textile technology firm STCH has successfully closed a $5.5 million pre-Series A funding round, signaling a significant shift toward deep-tech integration in the apparel supply chain.

Led by Omnivore, this capital injection aims to transition the sector away from its reliance on ‘trial-and-error’ R&D. While most fashion AI focuses on consumer styling, STCH targets the manufacturing core, utilizing a proprietary ‘Fabric GPT’ to reverse-engineer complex textiles. This system decodes fabric compositions - weight, texture, and finish -from digital inputs, allowing brands to bypass the traditional 20-iteration development cycle. By stabilizing the link between chemical inputs and tactile outputs, the firm is effectively industrializing precision manufacturing.

Strategic expansion and sustainable material substitution

The investment facilitates STCH’s entry into high-growth markets, specifically the United States and Spain, while expanding its R&D laboratory capabilities. A primary commercial objective is the development of biodegradable alternatives to petrochemical synthetics. Recent pilot projects have demonstrated the capacity to engineer cotton-based textiles that replicate the performance and hand-feel of polyester, removing the traditional trade-off between sustainability and quality. With a confirmed order book exceeding $15 million from global retailers like Shein and Being Human, STCH is positioning India as a centralized hub for AI-native textile innovation, offering a scalable alternative to fragmented traditional sourcing models.

AI-driven fabric R&D for global brands

STCH is a Bengaluru-headquartered Contract Development and Manufacturing Organization (CDMO) founded in 2025 by former Zetwerk executives. The firm provides AI-driven fabric R&D and supply chain orchestration for global apparel brands. Focusing on sustainable high-performance textiles, STCH currently scales production through a decentralized network of partner mills across Asia.

Cambodia T&A sector remains resilient with exports worth $3.8 billion in Q1, FY26

Cambodia’s T&A sector demonstrated significant resilience in Q1, FY26 by generating $3.8 billion in total export value. While the 7.7 per cent Y-o-Y increase reflects steady demand, the underlying narrative is one of strategic evolution beyond traditional assembly.

The Ministry of Commerce reports, apparel and textiles alone contributed $2.77 billion to this figure, a 7.6 per cent rise driven largely by the deepening integration of the Regional Comprehensive Economic Partnership (RCEP).

Industry analysts note, Cambodia is increasingly moving toward ‘high-value’ segments, with footwear exports rising by 11.8 per cent to $516 million. The shift from basic CMT (Cut, Make, Trim) to more complex functional apparel is what maintains our competitive edge in a tightening global market, notes Sophal Men, Regional Trade Consultant.

Supply chain resilience amidst global headwinds

Despite the growth, the sector faces a landscape of fluctuating logistical costs and stringent EU environmental mandates. To counter these pressures, Cambodian manufacturers are investing in solar-integrated production facilities to meet international ESG standards.

A case study of the Phnom Penh Special Economic Zone reveals, factories adopting green energy witnessed a 5 per cent reduction in operational overhead in early 2026. This transition is vital as travel goods exports also climbed to $513 million. By leveraging duty-free access to major markets and stabilizing labor relations through collective bargaining agreements, Cambodia is successfully positioning itself as a primary alternative to higher-cost manufacturing hubs in neighboring territories.

As a premier garment and footwear production hub, Cambodia serves global retail giants across North America and Europe. The nation is currently executing a five-year transformation plan to digitize supply chains and enhance labor skills. Following a decade of double-digit average growth, the sector now focuses on high-tech textile manufacturing to ensure long-term fiscal stability.

Arvind Ltd accelerates international expansion with Arvind Atelier acquisition

Arvind Limited has accelerated its international diversification strategy with the formal incorporation of Arvind Atelier (FZC) in Sharjah, United Arab Emirates. Established on April 20, 2026, this new subsidiary serves as a dedicated vehicle for the trading of ready-made garments and various textile products.

By securing an 80 per cent equity stake in the entity, the Ahmedabad-based conglomerate aims to capitalize on the UAE’s robust logistical infrastructure and its status as a primary commercial gateway to markets across Europe, Africa, and the Middle East. This move aligns with broader industry trends, as Indian textile exports to the UAE increased by 22.3 per cent in FY25-26, highlighting the region's increasing importance as a demand center.

Leveraging regulatory incentives and operational efficiency

The selection of the Sharjah Airport International Free Zone (SAIF Zone) provides Arvind with significant fiscal advantages, including 100 per cent foreign ownership and optimized tax frameworks. This structural decision is intended to mitigate the ‘triple squeeze’ of rising raw material costs, freight volatility, and tariff pressures that have recently impacted the sector's margins. In Q3, FY26, Arvind reported a consolidated revenue of Rs 2,372.64 crore, maintaining volume growth despite external cost headwinds. The UAE hub is expected to streamline the company's international supply chain, allowing for more agile distribution of its high-value woven fabrics and garments to global retail partners.

Leadership transition and long-term market integration

This expansion coincides with a pivotal leadership transition, as Punit Lalbhai assumed an executive role leading the textiles and apparel business on April 15, 2026. The new subsidiary represents a tangible step in the ‘Renovision’ philosophy - a strategy focused on shifting from domestic reliance to global dominance. As India concludes major trade agreements, including the recent FTA with the European Union in January 2026, Arvind's presence in the UAE positions it to better navigate preferential market access. By integrating a dedicated trading arm within a global logistics node, the company seeks to sustain its garmenting division's momentum, which recently achieved a record quarterly output of 10.7 million pieces.

Integrated textile excellence

Arvind Limited is a premier global textile-to-retail conglomerate specializing in denim, woven fabrics, and advanced materials. Managing a diverse portfolio from fiber to fashion, the company exports to over 120 destinations. With a focus on sustainable innovation and a 16.1 per cent ROCE, Arvind continues to lead India's high-value apparel manufacturing sector.

The New Rules of Resale: EPR turning secondhand into fashion’s strategic growth engine

The global fashion industry is facing a decisive regulatory and commercial reset. What began as a sustainability narrative around reuse and recycling is now evolving into a hard-edged business imperative, driven by the rise of Extended Producer Responsibility (EPR). Across major markets, particularly in Europe, policymakers are shifting accountability for textile waste from municipalities to producers, forcing brands to take ownership of the entire product lifecycle, from design and sale to post-consumer collection, sorting, reuse, and recycling.

For the secondhand apparel economy, this marks a inflection point. No longer positioned as a fringe sustainability channel, resale is emerging as a central infrastructure layer in the circular fashion value chain. The result is a reordering of how value is created, captured, and regulated in the global textile ecosystem.

The waste-recovery disconnect

The regulatory urgency behind EPR is rooted in the growing mismatch between textile production and recovery capacity. The EU now generates over 12 million tonnes of textile waste annually, yet less than 1 per cent of discarded textiles are recycled back into new garments. This imbalance has exposed the limits of the industry’s legacy linear model and accelerated the push toward enforceable accountability.

The implications for fashion businesses are big. As waste volumes rise and landfill restrictions tighten, secondhand and reuse channels are becoming the most immediately scalable route for diverting textiles from disposal. In commercial terms, this transforms resale from a brand extension strategy into a compliance-linked revenue stream.

Policies move from theory to enforcement

The new generation of EPR frameworks is distinguished by operational specificity. Mandatory separate textile collection across EU member states, which came into force in January 2025, has already begun to funnel substantially larger volumes of post-consumer garments into formal recovery systems.

This supply-side increase is being reinforced by eco-modulated fee structures, where producers pay differentiated contributions based on durability, recyclability, and material complexity. The financial logic is clear: garments designed for longevity and easy recovery become cheaper to manage, while low-durability fast-fashion products attract higher compliance costs.

The regulatory model is also beginning to influence upstream product development. Eco-design requirements are nudging brands toward mono-material constructions, repair-friendly formats, and longer-use garments. Meanwhile, the expected rollout of Digital Product Passports from 2026 introduces a new data layer that could materially improve fiber-level traceability and downstream sorting efficiency.

The supply boom comes with margin complexity

The most immediate impact on the secondhand market is an increase in feedstock volumes. However, market participants are finding that higher supply does not automatically translate into stronger profits.

Feature Business impact Volume A sharp rise in post-consumer textile inflows is expanding resale inventories. Durability A growing share of lower-quality fast-fashion garments is reducing average resale yield. Composition Complex fiber blends are making recovery and grading more expensive. Sorting Labour and technology intensity in sorting operations has increased significantly.

This table captures the paradox now facing secondhand operators: more garments are entering the system, but a larger proportion consists of low-durability, mixed-fiber products that carry weaker resale economics. In effect, EPR is improving access to supply while simultaneously exposing the quality deficits created by the fast-fashion era. For business operators, this means margin protection increasingly depends on superior grading intelligence, material recognition, and inventory discipline rather than simple scale.

Professionalisation of resale infrastructure

As compliance expectations rise, the secondhand sector is undergoing rapid professionalisation. What was once a fragmented ecosystem of thrift channels and opportunistic recommerce players is evolving into a more industrialised service layer for brands. Higher standards in traceability, waste reporting, and product-level transparency are driving investment into advanced grading methodologies, AI-assisted sorting systems, and data-led inventory engines. Automated fiber identification and robotics are becoming critical in processing higher textile volumes without proportionately increasing labour costs.

This technological shift is particularly important because reuse remains the most commercially viable circular pathway in the near term. While textile-to-textile recycling technologies continue to mature, resale and recommerce offer immediate value recovery with lower capital intensity.

The roadmap to 2028

The regulatory transition is unfolding through a phased timeline that gives brands and operators a narrowing window to build capability.

|

Timeline |

Milestone |

|

2022-24 |

EU Strategy for Sustainable and Circular Textiles introduced; Ecodesign framework approved. |

|

January 2025 |

Mandatory separate textile collection implemented across the EU. |

|

2026 |

Initial implementation of Digital Product Passports and expanded ecodesign requirements. |

|

2027-28 |

Full implementation of harmonized EPR schemes across EU Member States. |

The progression outlined in the table highlights why the next two years are critical. By 2026, traceability and design compliance will begin intersecting with resale infrastructure, while the 2027–2028 phase is likely to cement harmonised reporting, fee, and recovery obligations. For global apparel brands, waiting until full enforcement may prove commercially expensive.

Where the new value pools are emerging

The strongest opportunity lies in collaboration between brands, secondhand operators, and technology providers. Brand-controlled resale channels are rapidly gaining momentum as labels seek to retain ownership over product journeys, customer relationships, and EPR reporting outcomes. Proprietary resale storefronts, white-label recommerce partnerships, and embedded take-back ecosystems are all becoming strategic tools for compliance and customer retention.

At the same time, secondhand specialists are moving deeper into the enterprise services stack. Reverse logistics, sorting, grading, and take-back program management are increasingly becoming B2B revenue streams tied directly to brands’ regulatory obligations. This creates a new value pool where secondhand operators are no longer just merchants of used goods, but infrastructure partners in compliance-led circularity.

Compliance as competitive advantage

Extended Producer Responsibility is no longer a future-facing sustainability concept; it is fast becoming the operating system for fashion’s next phase of growth. For the secondhand apparel market, the shift introduces tighter standards, rising cost pressures, and a more formalised performance environment. Yet within this disruption lies an advantage. Businesses that invest early in traceability, AI-enabled sorting, reverse logistics, and transparent reporting can convert compliance from a cost centre into a moat. In that sense, EPR is doing more than rewriting the rules of the secondhand market, it is redefining who captures value in fashion’s circular economy.

Odisha accelerates textile ‘Farm-to-Fabric’ strategy with Rs 124 crore spinning investment

Led by Chief Minister Mohan Charan Majhi, the Odisha Cabinet has formally approved a Rs 124 crore investment for a modern spinning unit in Balangir district. Spearheaded by Shree Ambica Cotspin, this facility represents a critical shift in the state’s industrial policy to retain value within its borders. Despite a steady increase in regional cotton cultivation, Odisha has historically functioned as a raw material exporter, shipping high-grade cotton to spinning hubs in Tamil Nadu and Gujarat for processing. This new project aims to reverse that trend by establishing downstream processing infrastructure directly within the Kalahandi-Balangir-Koraput (KBK) region.

Integration of Industry 4.0 and regional supply chain resilience

Equipped with advanced spinning technology, the unit is designed to produce high-tenacity yarn for both domestic industrial markets and local handloom clusters. Beyond the immediate creation of 300 direct jobs, the facility acts as a catalyst for a proposed textile cluster in Western Odisha. Industry experts anticipate, localized yarn production will reduce logistics overheads for regional weavers by approximately 15–20 per cent. This project is the cornerstone of our 'farm-to-fabric' mission, notes Anu Garg, Chief Secretary. By aligning with India’s broader technical textile aspirations, the plant is expected to integrate IoT-enabled quality monitoring to meet international standards, facilitating direct export opportunities from the state's emerging manufacturing base.

Regional manufacturing specialization: Shree Ambica Cotspin

An Odisha-based enterprise with over 27 years of experience in the textile value chain, Shree Ambica Cotspin focuses on cotton ginning and yarn manufacturing, primarily serving the Eastern Indian market. Under its current expansion roadmap, the firm aims to leverage state incentives to modernize its spinning capacities and achieve vertical integration, significantly improving the financial returns for local cotton growers through direct procurement.

LSKD teams with Samsara Eco to integrate recycled nylon in collections

In a decisive move for the Australian performance apparel sector, Gold Coast-based activewear brand LSKD has formalized a ten-year strategic partnership with environmental technology firm Samsara Eco. Announced in April 2026, the deal centers on the integration of ‘infinite’ recycled nylon into LSKD’s core collections. Unlike traditional mechanical recycling, which degrades fiber quality over time, Samsara Eco’s proprietary enzymatic technology breaks down complex plastic waste into its original molecular building blocks. This process allows LSKD to produce high-compression leggings and high-intensity training gear that maintain the exact tensile strength and ‘second-skin’ handfeel of virgin nylon while significantly reducing carbon intensity.

Strategic market positioning and the 1 per cent sustainability mandate

The partnership arrives as the Australian activewear market is projected to reach a valuation of $13.2 billion by 2034, with nearly 41 per cent of consumers actively seeking eco-conscious fabric alternatives. For LSKD, which has seen explosive growth - transitioning from a $1.6 million business in 2019 to a global direct-to-consumer powerhouse - this long-term offtake agreement ensures supply chain resilience against the rising cost of sustainable raw materials. By locking in a decade of recycled feedstock, LSKD is positioning itself as a technical leader in the circular economy. Our mission is to be 1 per cent better every day, noted Jason Daniel, Founder, emphasizing, this collaboration moves the brand beyond seasonal ‘capsule’ drops toward a fully integrated, circular manufacturing model for its 200,000 global customers.

Founded in 2007, LSKD is an Australian-owned functional sportswear brand specializing in training, running, and adventure apparel. With a primary focus on the US and Australian markets, the company has achieved rapid scale through a wholly direct-to-consumer model. LSKD is currently expanding its global retail footprint while targeting 100 per cent sustainable fiber integration by 2030.