FW

Indian apparel leaders urge global brands to back supply chain modernization

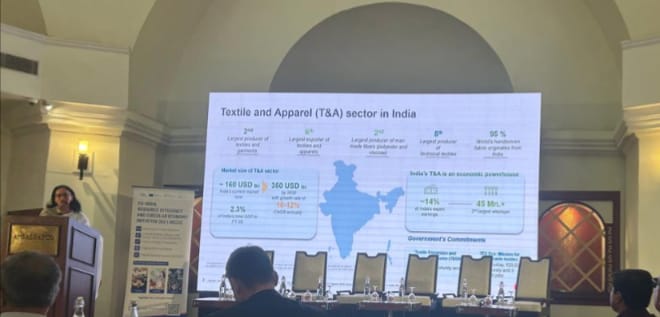

As India prepares to host the Bharat Tex 2026 mega-event in new delhi, the apparel export promotion council (AEPC) is shifting its focus toward aggressive supply chain integration. at a recent high-level roundtable in Bengaluru, Dr A Sakthivel, Chairman, AEPC, addressed representatives from 40 global retailers - including Walmart, PVH, and Ralph Lauren - regarding the industry’s critical technology and quality gaps. in a notable strategy shift, the council proposed active collaboration with the Taiwanese textile industry to import advanced synthetic yarn manufacturing technologies. Acknowledging that domestic fabric quality remains a hurdle, the leadership suggested that short-term imports of specialized materials may be required while India builds a more robust, traceable, and compliant internal ecosystem to meet the standards of premium global sourcing.

Trade agreements set the stage for a decade of industrial growth

The industry's current roadmap is heavily influenced by a suite of new free trade agreements (FTAs) with advanced economies, which leaders believe marks the beginning of a defining decade for Indian exports. Naren Goenka, Chairman, Bharat Tex emphasized, the current geopolitical climate offers India a unique window to emerge as the preferred alternative to traditional sourcing hubs. beyond mere manufacturing, the discussions highlighted a move toward circularity and mandatory traceability, reflecting the sustainability requirements of major buying houses like marks & spencer and C&A. by urging international brands to move beyond transactional relationships and proactively promote India’s capabilities, the council aims to transform the domestic apparel sector from a garment assembly hub into a technologically advanced, end-to-end global supply chain leader.

Lego leverages ogre-sized nostalgia to anchor 2026 growth strategy

The Lego Group has formally unveiled its inaugural Shrek collection, marking a pivotal expansion of its intellectual property (IP) portfolio into DreamWorks Animation’s multi-billion-dollar franchise. Scheduled for a June 1, 2026, global release, the collection features the flagship ‘Shrek, Donkey & Puss in Boots’ set alongside a specialized BrickHeadz line. This launch is a calculated move to capitalize on the ‘kidult’ demographic - adult fans who now account for approximately 25 per cent of all toy sales. By securing the Shrek license, Lego is tapping into a 25-year legacy of pop-culture relevance, strategically positioning these sets as high-margin collectibles rather than simple playthings

Financial momentum and supply chain localization

This product rollout follows a record-breaking FY2025, where Lego reported a 12 per cent revenue increase to DKK 83.5 billion ($12 billion), significantly outperforming a global toy market that grew by only 7 per cent. To support this aggressive product pipeline, which sees nearly 50 per cent of its 860-item catalog refreshed annually, the company is finalizing a new full-scale manufacturing facility in Virginia, USA, slated for 2026 completion. This localization effort is designed to shorten lead times for North American retail partners and mitigate the 30 per cent increase in logistics costs observed across the consumer goods sector over the past 24 months.

Omnichannel resilience amid discretionary shifts

As retail shifts toward ‘cozy culture’ and tech-free tactile experiences, Lego is doubling down on its ‘destination retail’ model, having surpassed 1,050 branded stores worldwide. The Shrek collection serves as a primary driver for these physical touchpoints, aiming to sustain the 16 per cent consumer sales growth reported last year. Despite inflationary pressures on discretionary spending, Lego’s ability to maintain operating margins near 26 per cent is attributed to its tiered SKU strategy. By offering entry-level BrickHeadz at $25 alongside premium $130 builds, the brand effectively captures diverse consumer segments, ensuring industrial resilience in an increasingly volatile global apparel and lifestyle market.

Operational scale and revenue outlook

The Lego Group is a privately held global leader in construction toys, operating in over 120 countries with a heavy focus on the US, China, and Western Europe. Through its partnership with Universal Products & Experiences, LEGO is scaling its licensed portfolio to drive toward a projected DKK 90 billion revenue target by 2027. Founded in 1932, the company recently achieved a milestone of using 52% renewable and recycled materials in its bricks, aligning financial growth with aggressive sustainability mandates.

From voluntary pacts to binding impact: The DST strategic transition

The German Partnership for Sustainable Textiles has officially completed its structural evolution into Dialogue and Impact for Sustainable Textiles (DST). Effective April 2026, this transition signals a fundamental departure from the voluntary commitment frameworks that defined the previous decade. As the European Union’s Corporate Sustainability Due Diligence Directive (CSDDD) begins to anchor legal liabilities for apparel brands, the DST is repositioning as a technical implementation platform. The objective is to convert high-level policy into shop-floor reality, moving beyond reporting to active risk mitigation in global supply chains.

Resource mobilization for supply chain resilience

A critical pillar of the DST relaunch is the ‘Learning & Implementation Community,’ which shifts financial responsibility toward private sector participants. In a notable strategic change, member companies will now assume direct funding roles for field projects, particularly those targeting living wage gaps and chemical management. Current industry data suggests this shift is timely; nearly 74 per cent of consumers now indicate a willingness to pay a premium for verified, traceable apparel. By integrating the Digital Product Passport (DPP) readiness into its core mission, the DST aims to provide its members with a competitive edge in a market where 2027 regulatory deadlines are rapidly approaching.

Systemic integration of global rights holders

The DST framework introduces a more inclusive governance model that integrates local trade unions and rights holders directly into the decision-making process. Dialogue alone does not improve conditions; real impact requires companies to change purchasing practices, noted a representative from a leading civil society partner during the April kick-off event. This ‘2+2’ model - uniting industry, academia, and local stakeholders - mirrors successful Indo-German bilateral projects and focuses on scalable industrial solutions for environmental and social compliance.

Strategic evolution and performance

Formerly the Partnership for Sustainable Textiles (founded 2014), the DST is a multi-stakeholder network overseen by the German Federal Government (BMZ). It coordinates sustainability initiatives for the German and European apparel sectors, focusing on technical textiles and global supply chain transparency. With a membership base that has navigated the industry's $1.7 trillion global valuation, the DST now prioritizes CSDDD compliance and circular economy integration to drive long-term sector performance.

CCIC revives Indian handloom dominance with ‘Soul Threads’ heritage launch

The Central Cottage Industries Corporation of India (CCIC) has inaugurated its premier heritage designer collection, ‘Soul Threads,’ marking a decisive pivot in the state-run enterprise’s brand revival strategy. Unveiled on April 24, 2026, at Jawahar Vyapar Bhawan, New Delhi, the exhibition integrates three thematic pillars - Anek, Maati, and Punah - reimagining Khadi and traditional weaves through a contemporary lens. By blending cotton, silk, and eri silk with advanced retting and upcycling techniques, CCIC is addressing the ‘modern utility’ gap that historically hindered artisanal exports. This initiative is timely, as India’s textile exports grew to Rs 3.16 lakh crore in FY 2025-26, with the handicrafts segment (excluding carpets) leading value-added growth at 6.1 prer cent.

Market resilience and the global 'Vocal for Local' vision

The ‘Soul Threads’ showcase acts as a high-visibility commercial platform for rural artisans and women-led enterprises, aligning with India’s broader objective of achieving a US$ 100 billion export milestone by 2030. Despite a revenue consolidation to Rs 41.9 crore in the previous fiscal year, CCIC is utilizing its premium designer collaborations to insulate traditional crafts from the price volatility of synthetic alternatives. Soul Threads signals our commitment to bridging heritage with innovation, positioning our weavers for a global audience, states Akhilesh Kumar, Chairman, CCIC. With the India-EU FTA and UK CETA now facilitating preferential market access, the corporation is poised to leverage these heritage assets to capture rising demand in high-growth markets like the UAE (up 22.3 per cent) and Japan.

Established in 1976 under the Ministry of Textiles, CCIC is India’s apex organization for promoting and retailing authentic handlooms and handicrafts. Operating flagship emporia in major metros, it supports over 40 million artisans. Current growth plans focus on digital transformation and expanding the ‘Jute Mark’ and ‘Handloom Mark’ certified designer lines internationally.

New Era shifts strategy to hi-tech experiential commerce

New Era Cap Co has officially inaugurated its North American flagship store in the heart of Manhattan’s SoHo district, marking a pivotal shift in the brand’s retail strategy toward hi-tech, experiential commerce. Located at 300 Lafayette Street, the store serves as a physical manifestation of ‘phygital’ retail, anchored by a massive 17x20 ft street-facing digital screen that broadcasts real-time collaborations and marketing campaigns. This immersive vestibule transitions into a sophisticated showroom where floor-to-ceiling cap displays meet original wooden hat forms from the brand’s first factories. By blending state-of-the-art visual engagement with its 100-year legacy, New Era is moving beyond transactional sales to cultivate a ‘collector’s sanctuary’ that resonates with Gen Z’s preference for immediate ownership and in-store storytelling.

Customization as a growth catalyst

Central to the flagship’s appeal is ‘The Garage,’ an old-school haberdashery-style space dedicated to hyper-personalization. The facility features on-site cap blocking machines and heat seals for custom patch application, allowing customers to design one-of-a-kind gear. This focus on individual expression aligns with New Era’s 2026 financial trajectory; the brand is projected to see a revenue growth of 5-10 per cent this year, following a robust US$ 352 million performance in 2025. With official licenses for the MLB, NFL, and NBA, the store acts as a high-velocity fulfillment hub for exclusive drops. This flagship is the global epicenter for the brand, allowing it to connect with its fanbase through innovation and creativity, notes Chris Koch, CEO during the April 27 opening.

Supplier to global teams

A global sports and lifestyle brand, New Era is the official on-field cap supplier for Major League Baseball and the National Football League. Headquartered in Buffalo, New York, the company operates across North America, Europe, and Asia. With estimated annual revenues between US$ 1 billion and US$ 10 billion, it is currently expanding its footprint through flagship experiential centers and high-profile collaborations with partners like adidas and Formula 1.

Hugo Boss faces advocacy pressure to re-sign Pakistan Safety Accord

On the 13th anniversary of the Rana Plaza disaster, global advocacy groups, including Labour Behind the Label and the Clean Clothes Campaign, have intensified pressure on Hugo Boss to recommit to the Pakistan Accord for Health and Safety. While over 100 global retailers renewed the legally binding agreement in January 2026, the German luxury house and Polish retailer LPP are among the high-profile minority that is yet to sign the updated 2026-2029 framework. Campaigners argue, voluntary internal audits are insufficient, citing recent inspection reports from Pakistan that highlight persistent life-threatening risks, including obstructed fire exits and structural vulnerabilities, within the brand's established supply chain.

The economic imperative of binding safety standards

The Pakistan Accord has become a critical benchmark for the region’s US$ 4.4 billion export sector, covering approximately 474 factories and 550,000 workers. Data indicates, signatory brands have realized a 15.8 per cent increase in export value since 2024, as the Accord provides the transparency required by eco-conscious Western markets. Remembrance is hollow without enforceable protection, stated a representative from the Rana Plaza Solidarity Collective during a London protest on April 24, 2026. As the industry faces new climate-related health crises, the Accord’s mandate is evolving to include heat-stress protections, making brand participation essential for maintaining a resilient and ethically sound apparel manufacturing hub in South Asia.

International Accord Secretariat

The International Accord is the administrative body overseeing legally binding safety programs in Bangladesh and Pakistan. It facilitates independent factory inspections and worker grievance mechanisms for nearly 200 signatory brands. Following a strong 2025 performance, the Secretariat is now prioritizing geographical expansion into other major manufacturing hubs to standardize global apparel safety protocols.

Style3D accelerates Bangladesh’s RMG modernization at BTKG Expo 2026

Global leader in AI-driven 3D fashion solutions, Style3D is set to demonstrate its end-to-end digital garment workflow at the Bangladesh International Textile, Knitting, and Garment (BTKG) Expo 2026. Held at the International Convention City Bashundhara (ICCB) in Dhaka from April 29 to May 2, the showcase arrives as the Ready-Made Garment (RMG) sector faces mounting pressure from geopolitical supply chain disruptions. By integrating physics-based fabric simulation with GPU-accelerated rendering, Style3D enables manufacturers to slash physical sampling by up to 60 per cent. This shift is critical for Bangladesh’s ambition to reach a US$ 100 billion export target by 2030, as it allows factories to move from low-value basic items to high-margin, technically complex apparel.

Physics-based realism and commercial efficiency

The centerpiece of the exhibit is the Style3D Studio V8.0, which features advanced AI pattern generation and real-time drape prediction with a 95 per cent correlation to physical fits. For Bangladeshi exporters, this technology addresses the ‘time-to-market’ barrier, reducing design iterations from weeks to mere hours. Industry data for 2026 suggests, early adopters of virtual prototyping have realized a 40 per cent gain in workflow efficiency and a 70 per cent reduction in fabric waste. Digital twins are no longer optional; they are the baseline for a sustainable, responsive supply chain, noted a lead technology consultant. By replacing traditional physical samples with 4K-resolution digital assets, manufacturers can stabilize their bottom lines despite the rising costs of raw materials like Tossa jute and man-made fibers.

A unified platform

A premier provider of digital fashion infrastructure, Style3D offers a unified platform for 3D design, fabric digitization, and cloud collaboration. Serving global fashion houses and apparel manufacturers, the company focuses on reducing carbon footprints through virtual sampling. Growth plans for 2026 include deep integration with ERP and PLM systems across South Asian manufacturing hubs.

Style3D specializes in AI-powered 3D garment simulation and digital fabric libraries, primarily serving the global apparel and textile industries. With its core market in Asian manufacturing hubs, the firm is scaling its Enterprise API and virtual try-on tools. Backed by a 5.7% sector CAGR, Style3D aims to lead the transition toward a fully digitized, waste-free fashion ecosystem.

Bangladesh accelerates jute revival via private sector participation

In a strategic effort to reclaim the global competitiveness of the ‘Golden Fiber,’ the Bangladesh Government has moved to reopen six closed state-owned jute mills by October 2026 under private sector management. Announced by Khandaker Abdul Muktadir, Textiles and Jute Minister, this transition shifts the sector away from historically inefficient state-led operations toward a market-driven model. Each revived facility is projected to attract investments between Tk 200 crore and Tk 500 crore, specifically targeting the production of diversified, high-value jute goods. By leasing idle assets to private operators, the administration aims to modernize manufacturing infrastructure and meet the rising international demand for biodegradable packaging and technical textiles.

Technological integration and export diversification

The government is simultaneously deploying an integrated agricultural framework to enhance fiber quality and yield. A foundational feasibility study, ‘Production and Distribution of Advanced Technology-based Jute and Jute Seeds,’ is currently underway, with full-scale implementation scheduled for November 2026. This initiative focuses on stabilizing the supply chain for 138 export markets, including the US and EU, where eco-conscious apparel brands are increasingly replacing synthetic materials with jute-blended yarns. Despite recent raw material price volatility, with Tossa and Meshta varieties seeing premiums of up to US$ 60 per metric ton, the mandate to digitize testing labs in Dhaka and Khulna ensures that Bangladesh’s 282 types of jute products adhere to rigorous global quality benchmarks.

Promoting diversified exports

The Bangladesh Textiles and Jute Ministry oversees the nation's jute and apparel sectors, contributing over 10 per cent to the national GDP. Focused on LDC graduation by late 2026, it promotes diversified exports through the Jute Diversification Promotion Center (JDPC). Their growth strategies emphasize public-private mill leases and a US$ 100 billion total export target by 2030.

Boatriders to capitalize growth in Parisian youth fashion with a new unified popup

The arrival of the Boardriders multi-brand concept at Citadium Caumartin marks a decisive move to consolidate action sports lifestyle brands under a singular, high-energy retail umbrella.

By integrating iconic names like Quiksilver, Billabong, and Roxy into a unified pop-up environment, the group is capitalizing on the seasonal growth in Parisian youth fashion. This installation serves as a strategic testing ground for a more cohesive retail identity, moving away from fragmented single-brand stores to a lifestyle-centric platform. Market analysts observe, this ‘house of brands’ approach allows for higher cross-selling opportunities, as consumers increasingly seek out curated heritage labels that define the surf and skate culture.

Strategic positioning amid global brand transitions

This retail activation coincides with a broader realignment of the Boardriders portfolio following its acquisition by Authentic Brands Group (ABG). The Citadium pop-up is a prime example of ABG’s licensing-led expansion model, aimed at maintaining brand heat while optimizing physical overhead. By securing prime real estate in the heart of Paris, the group is leveraging high footfall to drive its FY 2026 revenue targets. A sector specialist notes, the goal is to maintain the authentic core of surf culture while professionalizing the retail experience for a global metropolitan audience. This move effectively bridges the gap between technical boardshorts and mainstream streetwear, positioning the brands to capture a larger share of the European lifestyle market.

A leading global lifestyle and sports company, Boardriders Action Sports designs and distributes branded apparel, footwear, and accessories. Their portfolio includes Quiksilver, Billabong, and Roxy, targeting the surf, skate, and snow sectors. Now under Authentic Brands Group ownership, the firm is scaling its global licensing reach to enhance profitability and market presence.

Beyond the DTC Rush: Levi’s hybrid channel strategy sets a new retail benchmark

The global apparel sector is entering a phase where channel strategy is no longer a tactical lever but a core determinant of profitability. Levi Strauss & Co. has emerged as a defining case study in this shift, reporting that direct-to-consumer (DTC) channels now account for 52 per cent of its total revenues in the first quarter of fiscal 2026.

This milestone is not merely symbolic. It reflects a disciplined rebalancing of distribution, where digital platforms and company-operated stores scale in tandem with a still-expanding wholesale network. With quarterly revenues rising 14 per cent to $1.74 billion, Levi’s performance signals a move away from the industry’s earlier DTC at any cost focus to a more measured, hybridized commercial architecture.

Reframing the channel debate

The difference in channel strategies across global sportswear and denim majors has become increasingly pronounced. Nike, for instance, pursued an aggressive DTC shift by sharply reducing wholesale partnerships. While this initially increased margins and brand control, it eventually created distribution voids and inventory imbalances, forcing a relook and a renewed emphasis on wholesale partnerships by late 2025.

Levi’s, under CEO Michelle Gass, has taken a different route. The company’s ‘DTC-first but not DTC-exclusive’ philosophy has enabled it to scale its owned retail footprint now over 1,200 stores, without eroding wholesale productivity. Notably, wholesale revenues grew 12% during the quarter, underscoring that DTC expansion has been demand-led rather than substitution-driven. This distinction is critical. Rather than cannibalizing existing channels, Levi’s has increased total addressable demand, preserving its presence across diverse consumer touchpoints.

Growth anchored in channel synergy

The company’s regional performance shows how DTC and wholesale integration is driving growth across markets.

Table 1: Levi Strauss & Co. Q1 2026 revenue by region

|

Region |

Reported growth |

Organic growth |

DTC share growth |

|

Americas |

+9% |

+7% |

+10% |

|

Europe |

+24% |

+10% |

+19% |

|

Asia |

+13% |

+12% |

+18% |

|

Global Total |

+14% |

+9% |

+16% (Total DTC) |

The table highlights a dual-engine growth model. Europe emerges as a standout, combining strong reported growth with a sharp increase in DTC penetration, indicating successful premiumization and retail expansion. Asia, meanwhile, shows balanced organic growth and rising DTC contribution, reflecting both market maturity and digital adoption. Importantly, the Americas, Levi’s most established market continues to deliver steady gains, suggesting that the hybrid model is resilient even in saturated environments.

Monetizing brand control without overreach

Levi’s channel strategy is closely tied to its margin profile. The company reported a gross margin of 61.9 per cent, supported by disciplined pricing and reduced reliance on promotions. While operating margins reduced slightly to 11.4 per cent due to planned marketing investments and tariff pressures, the higher DTC mix is acting as a structural buffer against volatility.

The company’s ‘Behind Every Original’ campaign has increased brand equity, driving a 17 per cent increase in organic e-commerce and a 7 per cent rise in comparable store sales. This shows an advantage of DTC channels: the ability to directly translate brand storytelling into measurable commercial outcomes.

Equally significant is inventory management. Levi’s inventory grew by just 4 per cent, a stark contrast to the double-digit overhangs seen across the sector in recent cycles. By maintaining tighter control over demand signals through its owned channels, the company has avoided the markdown-heavy corrections that have eroded margins for many competitors.

Lessons from competing models

The Levi’s approach is increasingly influencing peers facing their own channel transitions.

Table 2: Comparative channel strategies in global apparel

|

Company |

Strategy |

Current outcome |

|

Nike |

Aggressive DTC push; reduced wholesale exposure. |

Rebuilding wholesale after distribution gaps. |

|

Under Armour |

Targeting 50% DTC via brand-owned stores. |

Transition underway amid revenue pressures. |

|

Adidas |

Rebalancing channels post inventory corrections. |

Stabilizing with mixed distribution strategy. |

|

Levi Strauss & Co. |

Balanced DTC expansion with simultaneous wholesale growth. |

Achieved 52% DTC with 12% wholesale growth. |

This comparison underscores a broader industry lesson: channel transformation is not merely about increasing DTC share, but about sequencing that transition without destabilizing distribution. Levi’s success lies in synchronizing both channels rather than prioritizing one at the expense of the other.

From denim specialist to lifestyle platform

Beyond channel metrics, Levi’s evolution reflects a deeper shift from a wholesale-driven denim manufacturer to a diversified lifestyle brand. The company’s presence across over 100 countries, along with its focus on women’s wear and international markets, is boosting its revenue base beyond core denim categories. It raised fiscal 2026 adjusted EPS guidance of $1.42-$1.48 signals confidence in both demand momentum and operational discipline. More importantly, it highlights the scalability of a model where channel strategy is embedded into product storytelling and consumer engagement.

Thus Levi’s 52 per cent DTC milestone is less about hitting a numerical threshold and more about redefining how brands interact with consumers. The company’s hybrid model demonstrates that owning the customer relationship does not require abandoning wholesale reach. As the apparel sector deals with demand volatility, inventory risks, and margin pressures, the Levi’s playbook offers a pragmatic path forward: build direct channels to capture value, but sustain wholesale networks to preserve scale. In an increasingly fragmented retail environment, it is this balance not extremity that is emerging as the true driver of resilience.