![]()

FW

The global textile chemical market is anticipated to increase at a CAGR of four per cent from 2016 to 2024. The fast growing markets are: China, Vietnam, Bangladesh and Malaysia who are triggering demand. Asia Pacific is the leading market for textile chemicals by revenue which accounted over half of the gross revenue in the world over the past couple of years.

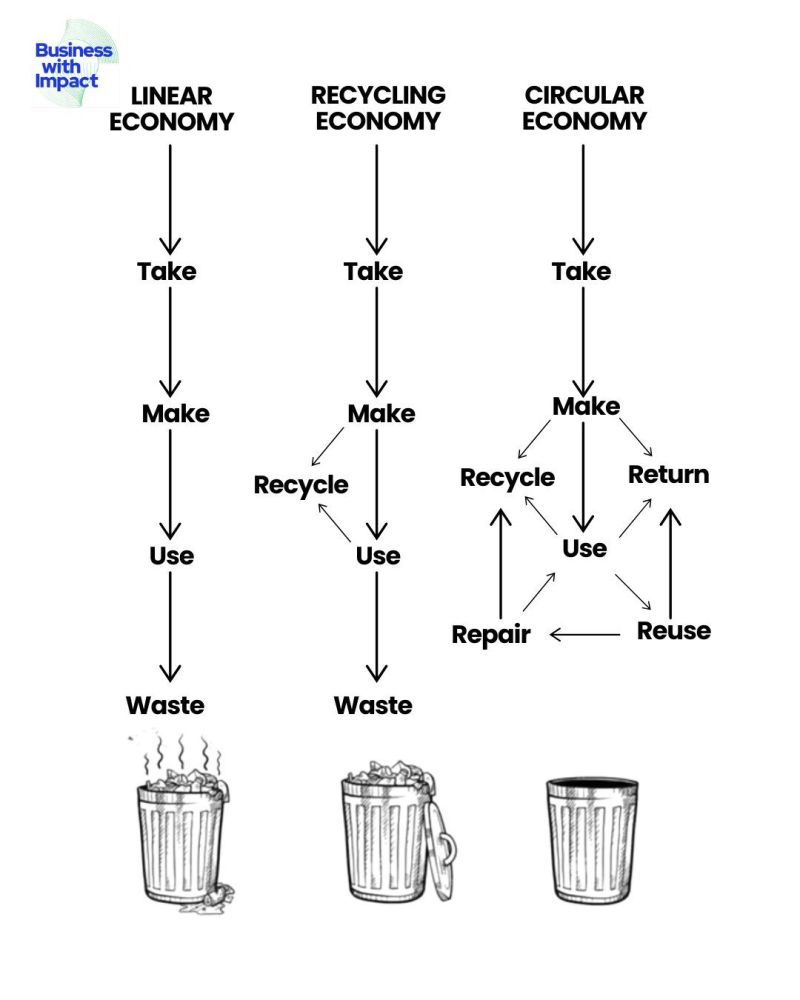

Textile chemicals are specialty chemicals in demand due to an increase in the variety of fabrics manufactured. These chemicals give fabrics better quality, flexibility and durability. They are a crucial part of the textile industry and play a vital role in manufacturing different type of fabrics like water resistant fabrics.

The global textile chemical market is segmented as surfactants, desizing agents, colorants and auxiliaries, coating and sizing chemicals, yarn lubricants and finishing agents. According to its applications the market is further segmented into home furnishing, apparels, industrial and others.

However, the major restraining factor for textile chemicals market is its harmful effects on the environment. The textile manufacturing process includes consumption of large volumes of water and specialty chemicals for dyeing, washing, bleaching, desizing and other processes. These chemicals contain surfactants and other toxic material which can cause potential harm to the environment.

Regional textile industries have been hit hard due to asurge in the cost of production and increasing competition from international players. Fluctuations in cotton prices and poor quality cotton in the region have also made trade difficult for textile mills. Industry experts said despite a drop in cotton prices, textile mills don't benefit. Textile mill owners, the textile market is in a depressive state and they cannot compete internationally because countries like Bangladesh, Vietnam and Pakistan offer garments at cheaper rates. Rising power costs, higher minimum wages and sluggish demand for garments from overseas buyers has dampened market sentiment. Moreover, strong Indian currency has also affected sales of textile mills in the country. Due to non-competitive prices and a surge in competition from competitors, demand for garments from overseas markets has dropped. Experts say benefits given by governments in rival countries such as subsidies and economic power supply have made their products popular in the global market.MC Rawat, secretary, Madhya Pradesh Textiles Mills Association points out textile industries in the region are reeling under the high pressure of increased labour wages and power costs making their products expensive against rival countries. Textile mills are hesitate to build up stock and conduct business hand to mouth because they lack knowledge about tax slabs under GST. A section of industries said that the lack of clarity on GST has also hurt business in the region.

Pakistan will re-impose a four per cent customs duty and five per cent sales tax on cotton imports. The decision will boost the confidence of domestic cotton growers during the upcoming sowing season. A decline in cotton production last season had forced a withdrawal of import duty and sales tax.

Pakistan's cotton consumption is pegged at around 15 million bales while it produces around 10.5 million bales. The country is the third largest raw cotton exporter but has been an importer for the last two years. Last year Pakistan imported around 2.7 million bales from India.

Meanwhile, the quantity of urea approved for exports has been increased from the existing 3,00,000 tons to 6,00,000 tons. Sufficient production and inventory of urea is anticipated during the kharif 2017 thus allowing for exports. Subsidies will be given on 19 commodities to provide relief during the upcoming holy month.

Arrow Textiles is a leading Indian manufacturer of specialty textiles in India. The company manufactures woven labels, fabric printed labels, elastic and non-elastic tapes. These products form a part of garment packaging products and are used for apparels and made-ups such as terry towels and home furnishings.

The company, founded in 1983, specializes in offering quick solutions and samples and can handle a variety of products as well and can communicate easily by using web-based ERP software. It is the preferred choice of many leading Indian brands, both for hosiery and outer wear.

Arrow has a manufacturing unit in Nasik with an installed capacity of 18 woven label looms, seven printed label machines and 59 woven tapes looms. It markets its products through depots located in Bangalore, Mumbai, Delhi and Tirupur.

The company’s key products are underwear name waistband elastic, woven inner elastics for garments, printed woven elastics, woven tapes, fabric printed labels, woven labels and 100 per cent cotton twill tapes.

The company’s relatively high gross and pre-tax margins suggest a differentiated product portfolio and tight control on operating costs relative to peers. It has relatively high profit margins while operating with median asset turns. Historical performance and long-term growth expectations for the company are largely in sync.

India’s spun yarn exports in March 2017 declined 47.6 per cent in volume terms and 39.3 per cent in value terms. In March 2017, 83 countries imported spun yarn from India, with Bangladesh at the top, accounting for 20.24 per cent of the total value, with imports plunging 41 per cent in terms of volume year on year and 32 per cent in value year on year. China was the second largest importer of spun yarns and accounted for around 17 per cent of all spun yarn exported from India. Exports to China were down 65 per cent in volume and 59 per cent lower in value.

Pakistan was the third largest importer of spun yarns, which saw volume rising 3.1 per cent and value rising 4.6 per cent. These three top importers together accounted for around 44 per cent of all spun yarns exported from India in March. Cotton yarn was exported to 71 countries with Bangladesh as the largest importer from India in March, followed by China and Pakistan. The top three together accounted for more than 49.35 per cent of cotton yarn exported from India.

Brazil, Dominican Republic, United Arab Emirates, Jordan and Madagascar were among the fastest growing markets for cotton yarn, and accounted for 3.47 per cent of total cotton yarn export value. Eleven new destinations were added for cotton yarn export, of which North Korea, Chile, Oman and Austria were the major ones.

Indian textile and garment companies eyeing trade co-operation with Vietnamese enterprises, said Indian Consul General in Ho Chi Minh City Smita Pant at a function to introduce the Textiles India 2017 in Vietnam.

Pant says, textile and garment is a leading industry where the two nations need to foster co-operation by promoting trade, attracting investment and increasing export turnover. Ronak Roughani, Vice President of the Synthetic and Rayon Textile Export Promotion Council (SRTEPC) of India adds apparels are a large proportion of India’s exports.

India’s export turnover of textile and garment materials to Vietnam in recent years has seen an average increase of about 20 per cent a year. This is a good time for Vietnamese and Indian textile and garment firms to enhance investments, export materials and technical assistance for mutual benefit.

However, Vietnam is also one of the world’s leading importers of fabric and materials. Shortage of high-quality materials for production is the biggest barrier to Vietnam’s textile and garment industry, hindering it from taking advantage of free trade agreements.

Pham Xuan Hong, Chairman of the HCM City Association of Garment Textile Embroidery and Knitting (AGTEK) observed Vietnamese textile and garment firms appreciate the quality and competitive price of materials from India, stressing co-operating with India businesses is an effective measure to diversify material supply resources for Vietnam.

Discussing issues such as ‘youth, technology & growth’, the World Economic Forum ASEAN forum, attracted global leaders. At the WEF ASEAN forum held in the Cambodian capital of Phnom Penh from May 10-12, discussions focused on obstacles that will have to be overcome should the region see true, equitable growth. Infrastructure, governance and open dialogue were key components of the talks but with a widening wealth gap, and a burgeoning Fourth Industrial Revolution that threatens to leave even more of the region’s vulnerable population behind, ASEAN has its work cut out.

China has long been, in the words of Cambodian Prime Minister Hun Sen, ‘strategic partner’ of ASEAN. ASEAN benefits a lot from this relationship. For years, the US pivot to Asia helped shape geopolitics, investment and development in Southeast Asia. But with anticipated disengagement and mounting protectionism from President Donald Trump’s administration, a lot of discussion centered around what impact that shift may have on China’s role in the region. At a panel titled ‘Southeast Asia and the Big Picture’, speakers grappled with the question of what that shift may mean.

China’s reigning stronghold

Will there be ‘a pivot to China’, asked Jamaludin Ibrahim, head of Axiata Group in Malaysia. With the ‘US disengaging from the region does China fill the void?’ Every country in Southeast Asia welcomes Chinese investment, wants to be part of One Belt One Road, George Yeo, visiting scholar at the Lee Kuan Yew School of Public Policy, told the audience at the panel. There is no question of the economic potential China allows for in the region. Yeo stressed most ASEAN countries prefer to remain promiscuous and did not want China to be their exclusive partner.

ASEAN and the Fourth Industrial Revolution

Singapore is ranked 9th out of 187 countries for education, Myanmar is ranked 150th. In a region with vast wealth, development and educational disparities, many at WEF ASEAN asked what impact the Fourth Industrial Revolution of rapid digital and technological change will have. Participants agreed now is a make or break time if Southeast Asia is to prosper from the Fourth Industrial Revolution. The Fourth Industrial Revolution truly will bring benefits for people in all countries. But one should not forget that technologies will also create risks for jobs, said Prime Minister Hun Sen. ASEAN must adopt appropriate measures to ensure sustainability of labour market — quality education aiming at increasing labour skills, said Laos Prime Minister Thongloun Sisoulith.

A question frequently raised was whether ASEAN countries needed to replicate an EU-style policy of unification. At a panel discussing the connectivity conundrum for the region, connecting the ASEAN countries through transportation, telecommunications and critical infrastructure networks, political unification was considered a necessity. Across the region, it could facilitate trade, enable sharing of resources, and develop consistent policies for environmental protection to continue the economic, political and social development of the region. It’s right to make the case for connectivity as a way to reduce inefficiencies, Anna Marrs, CEO for the Standard Chartered Bank, told the audience.

An important first step in making this happen was for governments to come together to create consistent policy and processes, including trade policies and cross-border employment, ensuring the private sector is encouraged to invest and do business in the region. Sun Chanthol, the Cambodian minister of public works and transport, explained that for Cambodia in particular this was an important step in the process to continue the expansion of infrastructure investment and open his country to the region and the world.

A sudden spurt in cotton futures in international market over the last three days has left cotton traders perplexed in India. While the fundamentals support a possible bearish trend owing to wider sowing of the fibre crop, the recent rally in international markets is encouraging farmers towards further cotton cultivation.

On the Intercontinental Exchange (ICE) in the US, the cotton futures for July 2017 contract rallied by about 12 per cent in just three sessions to hit a high of 85.32 cents per pound on Monday a level not seen in more than two years. This prompted ICE to increase the margin requirements thereby indicating speculators’ play behind the sudden spurt.

On ICE the cotton July futures cooled off a bit to 83.99 cents on Tuesday. This sent out a bullish sentiment in the global cotton markets including India, a key global cotton player. The spot rates on Indian markets rebounded by nearly 1,000 per candy (each of 356 kg) to trade at 42,700 on Tuesday. On the MCX, cotton futures for the immediate month contract quoted at 21,170 per bale after hitting a high of 21,260. In March, cotton futures had quoted at 21,060.

Experts say the rally is artificial and will be short-lived. The intergovernmental group, International Cotton Advisory Committee (ICAC), had projected an increase of about 1 per cent in cotton production globally to 23.1 million tonnes in 2017-18. As per the initial estimates, cotton sowing in India has been estimated to increase by 10-12 per cent, while in some pockets, the cotton area may go up by as much as 20 per cent over last year. The trigger for the sharp surge in cotton area is the higher prices as compared to the other alternate kharif crops, such as paddy and pulses.

International buyers, who were to settle their positions, continued making further positions in cotton futures for some reasons. This led to the spurt in prices. In the Indian context, due to such higher international prices, our imports will shrink more than the estimated. So, the country may feel the shortage of cotton around July and those holding cotton stocks may get 46,000-47,000 per bale. But that would be a very short-term as we expect more acreage this year.

India's next generation FTA - the Economic and Technical Cooperation Agreement - with Sri Lanka seems to be running into rough weather. Sri Lanka's trade and industry has not been happy with the earlier FTA that was signed in 2000 with India. Sri Lanka’s exports to India have grown 275 per cent since 2005-06. And India's exports to Sri Lanka have grown 96.48 per cent during the same period.

Negotiations on both sides are on to iron out differences on the upgraded Free Trade Agreement of 2000 to include services, investment and technological trade. There are reasons for India to guard its flanks while negotiating a second generation free-trade agreement with Sri Lanka.

China has evinced interest in an FTA with Sri Lanka as well. This has given India pause, as it wants to see the details of that deal. This could include Chinese companies setting up manufacturing bases in Sri Lanka and using the India-Lanka FTA to push Chinese goods into India. In many segments, Chinese products have already flooded Indian markets.

Tariff and non-tariff barriers to protect local industries, visa regulations, entry barriers to investment are some of the important reasons South Asian regional trade has remained fragmented.

French companies continue to dominate the luxury market in sales, while Italian companies were the most numerous, also posting the strongest growth over last year. The global luxury industry is relatively resilient, with an average sales growth of 6.8 per cent compared to 2014. This increase in turnover marks a noticeable improvement in growth, too, up 3.7 per cent over the year prior, mainly due to favorable exchange rates.

LVMH is the world’s leading luxury company. The French conglomerate’s portfolio includes Louis Vuitton, Fendi and Céline. The LVMH group alone accounts for more than ten per cent of the total sales of all the top 100 companies.

LVMH is followed by the Swiss group Richemont and the American Estée Lauder. Ralph Lauren is 8th and PVH at the number 10 spot. Other US companies include familiar names like Michael Kors, at position 14 and Coach at 15. Fossil Group is at position 20.

French luxury companies experienced the strongest growth in 2016 at an average rate of 14.9 per cent. They also lead the country ranking in terms of sales with a total turnover of more than five billion dollars, achieved by just ten companies. Moreover, three of the ten largest luxury groups in the world are French (LVMH, Kering, L'Oréal Luxe) and account for more than 75 per cent of the sales of luxury products by companies based in France.

Italy is the leader in terms of the number of companies overall, with 26 Italian firms qualifying. However, their total turnover is only 16 per cent of the sales of all 100 companies. Leading the Italian contingent is Luxottica, followed by Prada and Giorgio Armani. Other new brands, some of which do not have typical luxury profiles, are brands like British labels Barbour, Ted Baker and Charles Tyrwhitt, German brands Marc O'Polo and Marc Cain, and French label SMCP (Sandro, Maje, Claudie Pierlot).