![]()

FW

The Show Miami, the city’s first-ever social fashion fair, is set to launch, bringing top brands, industry leaders, and fashion enthusiasts together for an immersive experience. Taking place at the Miami Beach Convention Center from March 17 to 19, the event aims to redefine fashion by merging commerce, creativity, entertainment, and community.

More than just a trade show, The Show Miami is a movement to position the city as a global fashion hub. Attendees will experience cutting-edge fashion presentations, interactive installations, insightful panel discussions, live music, and networking opportunities. “Our vision is to redefine how fashion is experienced, merging industry and culture in a way that’s never been done before in Miami,” said Ivan Herjavec, co-founder of The Show Miami.

The event will feature collections from leading brands such as Lacoste, Levi’s, Psycho Bunny, Sprayground, Perry Ellis, Original Penguin, True Religion, Cult of Individuality, Ed Hardy, and many more. Live art installations, including a graffiti artist in action, will add a creative edge. A state-of-the-art padel court will offer both professionals and attendees a chance to engage in the trending sport. DJ sessions by Palo Santo will provide daily entertainment.

Panel discussions will explore topics like AI in fashion, Miami’s fashion founders, and music’s influence on streetwear. The event also embraces a community-driven approach, with a fundraiser for Miami Dade College students reinforcing its mission of using fashion as a force for unity and support. Visitors can contribute by attending the event and purchasing exclusive products.

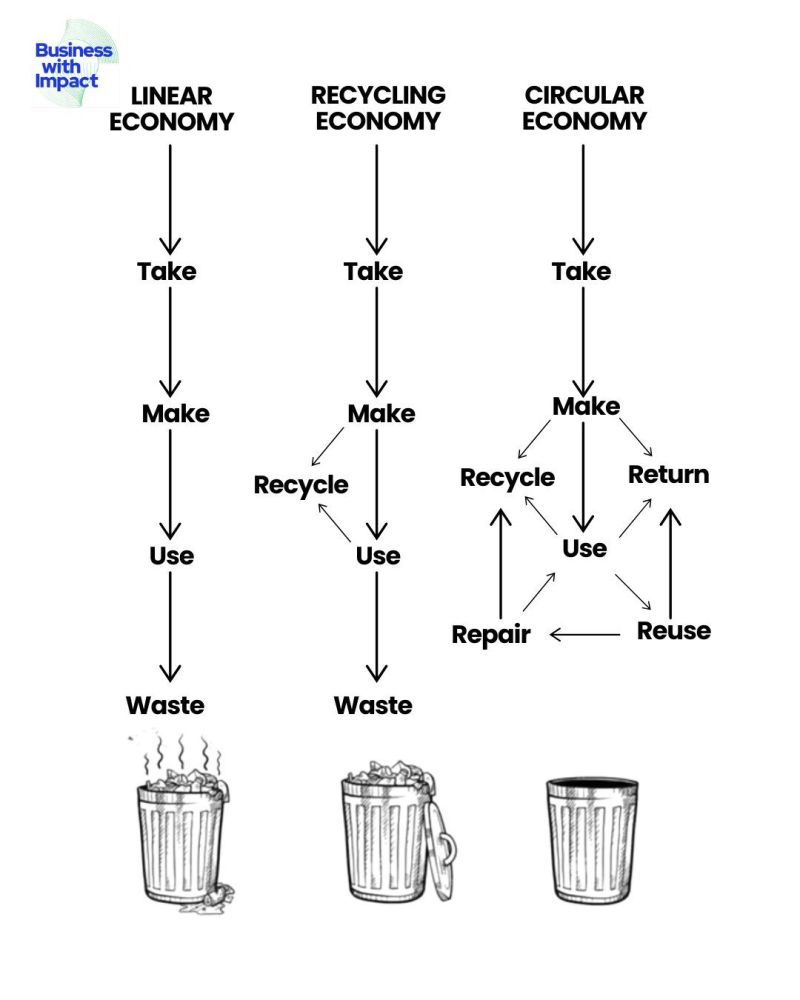

The Renewable Carbon Initiative (RCI) has released a detailed study analyzing Life Cycle Assessment (LCA) and carbon footprint standards concerning renewable carbon sources, including biomass, carbon capture, and recycling. Conducted by Nova-Institute, the study compares major sustainability frameworks, highlighting areas of consensus and divergence.

LCA is the key methodology for assessing environmental impacts, but its complexity and varying approaches challenge fair assessments, particularly for renewable carbon-based materials competing with fossil-based alternatives. The study evaluates key LCA frameworks, including ISO 14040/44, ISO 14067, the GHG Protocol, PACT’s Pathfinder Framework, and others relevant to industry and policy.

The findings indicate general agreement on biogenic carbon accounting, with most frameworks following the -1/+1 approach, except for PEF and RED III, which use a net-zero method. However, substantial differences exist in handling processes with multiple outputs and whether co-products can be credited through system expansion. Recycling methodologies also show significant variability.

The study comprises three reports: a 146-page assessment of LCA methodologies, a 36-page focus on recycling, and a 15-page non-technical summary for policymakers. RCI calls for clearer guidelines on critical aspects such as mass balance attribution and carbon capture utilization (CCU) to ensure consistency in sustainability assessments.

As industries shift toward circular carbon solutions, the study underscores the need for standardized LCA methodologies to create a level playing field for renewable carbon products. Policymakers and stakeholders must address methodological flexibility to enhance transparency and comparability in carbon footprint evaluations.

Leading knitwear manufacturers from Portugal to Pakistan trust Monforts Montex stenters for precision and automation in drying after dyeing and other essential processes.

“Knitted fabrics require delicate handling due to their higher elasticity compared to woven materials,” says Monforts Marketing Manager Nicole Croonenbroek. “Montex stenters ensure smooth processing with low, controlled tension and gentle thermal treatment. They also offer flexibility across various fabric qualities while improving energy efficiency.”

ATB - Acabamentos Texteis de Barcelos, one of Europe’s largest dyeing and finishing firms, dyes 36-40 tons of fabric daily for brands like Benetton, Inditex, and Mango. Since installing its first Monforts Montex stenter in 1990, ATB has added four more, each 2.8 meters wide and equipped with heat recovery units and advanced control systems for efficiency and reproducibility. The facility also operates Monforts Dynair relaxation dryers and an EcoApplicator.

Knitting at ATB is supported by Etevimol, another Barcelos-based firm, which became fully owned by the Mano family in 2024. Its 160 knitting machines are being relocated to ATB, with a €5 million investment planned for new equipment. ATB maintains a growing library of 10,000 fabric samples to quickly meet customer needs.

Pakistan’s Interloop, another major Monforts customer, started in 1992 with ten knitting machines and is now one of the country’s largest listed textile firms. It aims for $700 million in sales by 2026. Its latest Faisalabad facility produces 50 tons of knitted and dyed fabric daily, supporting 45 million garments annually. The 1.25-million-square-foot plant has the highest Leed score for its scale, using renewable energy and advanced water management.

“Monforts Montex stenters set the industry standard in precision, efficiency, and reliability,” Croonenbroek adds. “They offer unmatched durability, supported by our commitment to excellent customer service.”

The familiar sight of bustling clothing stores, once cornerstones of shopping malls and high streets, is fading. A chilling wind is sweeping through the apparel retail sector, leaving behind a trail of shuttered storefronts and bankruptcies. The so-called ‘retail apocalypse’, a term that has haunted the industry for years, is intensifying, particularly in the realm of clothing.

A statistical snapshot of decline

Data paints a stark picture. As per Coresight Research, in 2023, US retailers announced over 5,000 store closures, with a significant portion belonging to apparel and footwear. While this number is down from the pandemic highs, the trend of closures continues. In the first half of 2024, numerous brands have already announced significant downsizing.

"The landscape is undeniably shifting," says Deborah Weinswig, CEO, Coresight Research. "While the pandemic accelerated existing trends, the underlying issues – overexpansion, changing consumer behavior, and the rise of e-commerce – remain." Globally, the impact is being felt most acutely in the US and parts of Europe, where traditional retail infrastructure was most entrenched. However, even emerging markets are witnessing a recalibration as consumers increasingly embrace online shopping.

And here are some examples of the meltdown. For example, JCPenney, once a department store giant, JCPenney filed for bankruptcy in 2020, closing hundreds of stores. While it emerged from bankruptcy, its footprint is significantly reduced, reflecting the struggles of mid-market department stores. The brand’s inability to adapt quickly enough to the digital landscape and its struggles with brand identity were major contributing factors.

Similarly, recently, Express filed for bankruptcy and announced the closure of over 90 stores. This highlights the ongoing challenges faced by apparel retailers targeting younger demographics, who are particularly susceptible to online trends and fast-fashion alternatives. Bed Bath & Beyond is another example. While not strictly apparel, the collapse of Bed Bath & Beyond serves as a cautionary tale. Once a retail giant, its failure to adapt to online competition and its reliance on outdated business models led to its demise. This demonstrates the fragility of even established retail brands in the current climate.

Other notable closures/restructuring included the likes of Gap, Banana Republic and even fast fashion brands like Forever 21 that have gone through periods of significant store closures and restructuring in recent years, demonstrating that no sector of the apparel industry is immune.

Why the crisis?

There are several factors behind this perfect storm. E-commerce dominance is a major one. The rise of online shopping has fundamentally altered consumer behavior. Convenience, price comparison, and a vast selection have lured customers away from brick-and-mortar stores.

Meanwhile, consumers too are increasingly prioritizing experiences over material possessions. Sustainability and ethical sourcing are also gaining importance, putting pressure on traditional retailers to adapt. Many retailers expanded aggressively during periods of economic growth, accumulating significant debt. The pandemic and subsequent economic uncertainties exposed these vulnerabilities.

Also, rising inflation and economic uncertainty are forcing consumers to tighten their belts, leading to decreased spending on discretionary items like apparel. The rise of fast fashion and now ultra fast fashion like Shein, has put immense pressure on traditional retailers to keep up with trends and offer competitive prices. As Neil Saunders, Managing Director, GlobalData Retail opines, “The consumer has evolved, and retailers must evolve with them. Those who fail to embrace digital innovation, curate compelling in-store experiences, and offer value-driven propositions will continue to struggle."

The future of apparel retail

The ‘retail apocalypse’ is not necessarily the end of brick-and-mortar stores. Rather, it signifies a period of profound transformation. The future of apparel retail lies in first the seamlessly integrating online and offline experiences. Adopting experiential retail that offer unique and engaging in-store environments. Leveraging data to understand customer preferences and tailor offerings. Embracing environmentally and socially responsible business models and reducing store footprints and focusing on curated assortments.

A recent survey by product auditing firm QIMA reveals the persistent quality and failure issues plaguing the global garment industry, a disconcerting trend of declining standards amidst escalating pressures. This isn't just a matter of frayed seams; it's a systemic issue impacting consumer trust, brand reputation, and the fabric of the global supply chain.

The QIMA report: A stark reality check

QIMA's latest quality control report, analyzing data from thousands of inspections and audits conducted globally, indicates a worrying uptick in defect rates across various garment categories. While specific numerical data points fluctuate depending on the region and product type, the overall trend points to a consistent challenge in maintaining quality. "We've observed a recurring pattern of issues related to fabric defects, stitching inconsistencies, and sizing discrepancies," says Sebastien Breteau, CEO of QIMA. “The pressure to deliver at lower costs is undeniably impacting the overall quality control processes.”

The report highlights common defects:

Fabric flaws: Holes, stains, and uneven weaves, often indicating subpar raw material sourcing or inadequate quality checks.

Stitching irregularities: Skipped stitches, loose threads, and uneven seams, point to potential issues with machinery maintenance or operator training.

Sizing inconsistencies: Variations from specified measurements, leading to consumer dissatisfaction and increased return rates.

These findings are corroborated by anecdotal evidence from consumer forums and online reviews, where complaints about poor garment quality are rife.

The price-quality paradox

One of the most significant factors contributing to this decline is the relentless pressure to drive down prices. In a hyper-competitive market, brands are constantly seeking ways to reduce costs, often at the expense of quality. This is particularly evident in the sourcing of fabrics, where cheaper alternatives may be used to meet aggressive price targets. There's a constant tension between cost and quality, say sourcing managers. They say, to meet the price points demanded by retailers and consumers, sometimes they have to compromise on fabric quality. This can lead to issues with durability and appearance.

This pressure is increased due to fast fashion, where rapid production cycles and low prices are paramount. The focus on speed and affordability often leaves little room for rigorous quality control, creating a breeding ground for defects. For example, the Rana Plaza incident in Bangladesh in 2013; while the accident was a structural failure, it highlighted the risks of cutting corners to meet low price demands, and the pressures placed on manufacturing facilities. Even though much has changed since, price pressures still remain.

Navigating conflicting demands

Consumers are increasingly demanding both affordability and quality. However, they are often unaware of the trade-offs involved in achieving these seemingly contradictory goals. This creates a dilemma for brands, who must balance the need to offer competitive prices with the imperative to maintain quality standards.

The rise of e-commerce has further complicated the situation. Online shoppers often rely on visual cues and product descriptions, which may not accurately reflect the actual quality of the garment. This can lead to disappointment and returns, impacting brand reputation and profitability.

"Consumers want value for money, but they also want products that are durable and well-made," says a retail analyst. "Brands need to be transparent about their sourcing and manufacturing practices to build trust and avoid consumer backlash."

The marketplace is also seeing a rise in sustainable fashion, where consumers are willing to pay a premium for ethically sourced and environmentally friendly products. This trend could potentially shift the focus from price to quality and sustainability, but it remains to be seen whether it will have a significant impact on the broader industry.

Towards a more sustainable quality model

Addressing the quality challenges facing the garment industry requires a multi-faceted approach. Brands need to invest in robust quality control systems, from raw material sourcing to final product inspection. Supply chain transparency is also crucial, allowing consumers to make informed choices about the products they purchase.

Also, a shift in consumer mindset is needed, moving away from a focus on low prices towards a greater appreciation for quality and durability. This requires education and awareness campaigns to highlight the true cost of cheap clothing, both in terms of environmental impact and ethical considerations. Ultimately, the future of the garment industry depends on its ability to balance the demands of affordability and quality, creating a more sustainable and responsible model that benefits both consumers and producers.

With inflation staying high and interest rates surging, consumers have become more cautious with their spending. As a result, many retailers have struggled to stay afloat, leading to a wave of store closures and bankruptcies since the 2020 shutdowns. The wedding industry has also faced lasting challenges, with many venues and vendors still grappling with fewer bookings even years after the pandemic disrupted large-scale celebrations.

David’s Bridal, once the dominant force in wedding retail, felt the impact firsthand. The shift toward smaller, budget-conscious celebrations and reduced demand for formal attire contributed to its second Chapter 11 bankruptcy filing in April 2023. After restructuring, the company was acquired by Cion Investment Corp., allowing around 200 stores to remain open.

Now, under new CEO Kelly Cook, David’s Bridal is transforming into a media-driven business. Its Pearl Media Network leverages content to attract customers and generate advertising revenue.

The company is also expanding its online marketplace beyond wedding dresses to include men’s suits, rentals, swimwear, and occasion wear through a drop-ship model. This strategy reduces costs by eliminating excess inventory and store expansions while enabling rapid scaling.

Although David’s Bridal serves 90 per cent of the US bridal market, it captures only a third of dress sales. By focusing on media and e-commerce, the company aims to strengthen its financial position and drive profitability, adapting to an evolving wedding industry.

Boohoo Group is rebranding as Debenhams Group and revamping its business model to navigate the challenging online retail landscape. CEO Dan Finley, who took charge recently, announced the transformation, inspired by the successful turnaround of Debenhams, which Boohoo acquired in 2021.

Debenhams now generates gross merchandise value (GMV) of 654 million pounds, with net sales of 205 million pounds and a 12 percent EBITDA margin. Finley aims to replicate this success by adopting a ‘stock-lite and capital-lite’ marketplace approach for the company’s youth brands, including Boohoo, PrettyLittleThing, and BoohooMan, which have a combined GMV of over 1.5 billion pounds.

The restructuring includes heavy discounting to reduce stock, shutting the US distribution center, selling London offices, and cutting costs. Karen Millen has been repositioned as a premium digital-first brand. Full-year GMV fell 10 percent, with revenue down 16 percent to 1.22 billion pounds.

Market analysts remain skeptical, citing Shein’s dominance and shifting consumer trends. Shares dropped 4.61 percent to 0.26 pounds following the announcement. The name change requires shareholder approval on March 28. Finley remains optimistic, calling the move a ‘defining moment’ for the company’s future.

Bizpando AG, in collaboration with the Aid by Trade Foundation (AbTF) and the International Cotton Advisory Committee (ICAC), has launched a project to promote carbon credits in cotton farming. The initiative aims to equip African smallholder farmers with sustainable agricultural techniques and digital tools to improve soil quality, sequester carbon dioxide, and generate additional income.

By implementing climate-smart practices such as biochar application, minimal tillage, and cover cropping, farmers can sequester up to 5.75 tonnes of carbon dioxide per hectare annually. This approach enhances soil fertility, reduces reliance on pesticides and fertilizers, and increases crop yields. Cotton growers certified under the Cotton made in Africa (CmiA) standard will benefit from selling carbon credits, creating new revenue streams while lowering costs.

"Our approach not only protects the environment but also boosts cotton farmers' productivity and income," said Tina Stridde, Managing Director of AbTF. ICAC’s Chief Scientist Keshav Kranthi highlighted biochar’s role in enhancing soil structure, water retention, and microbial activity, contributing to long-term carbon storage.

Bizpando will lead the digital implementation, developing a GPS-based system to accurately map farmland, prevent double counting, and ensure transparent carbon credit validation. The platform will facilitate the issuance and sale of credits, ensuring direct payouts to farmers. "By integrating digital solutions, we maximize financial benefits for farmers while cutting administrative costs," said Jasper Bhaumick, CEO of bizpando AG.

In the coming months, the partners will enhance the platform, secure certifications, and initiate training programs. The first carbon credits are expected by 2026, with groundwork already underway.

Consumption of cotton yarns by the UK is projected to increase at a 1.1 per cent CAGR to 7.7,000 tons from 2024-2035. This growth will mostly be driven by consistent demand, despite recent declines. The total value of the UK cotton yarn market is projected to grow to $43 million by 2035.

In 2024, UK’s total cotton yarn consumption declined by 6.7 per cent to 6.8000 tons while revenues in the market declined by 12.2 per cent to $38 million.

Domestic production of cotton yarn in the UK remains minimal, with approximately 32 tons produced in 2024, mirroring the previous year. Production has steadily decreased over the past decade.

To meet its cotton yarn demand, the UK relies heavily on imports. In 2024, its imports declined by 8.6 per cent to 7.8000 tons, valued at $45 million. Key suppliers include Pakistan, Spain, and Turkey, with Egypt, Turkey, and India leading in value. The majority of imports are non-retail cotton yarn, both containing less than and more than 85 per cent cotton. Import prices averaged $5,719 per ton, varying significantly by product type and country of origin, with Egypt commanding the highest prices.

Exports of cotton yarn by the UK declined by 19.9 per cent to 1,000 tons to $38 million in 2024. Major export destinations included the United States, Lithuania, and Turkey. Notably, France witnessed the most significant growth in exports. Despite recent downturns, the UK cotton yarn market is expected to experience gradual growth, driven by consistent demand and strategic import relationships. However, domestic production remains low, and the market is heavily reliant on international trade.

Turkey’s leading textile manufacturer, Yunsa’s net profit declined to 36.6 million lira in FY24 as against 785.8 million lira recorded in the previous year.

Yünsa’s annual revenues also contracted to 1.94 billion lira in FY24 from 3.16 billion lira in FY23. This substantial decline was an outcome of the ongoing challenges in the textile sector, including global demand fluctuations, inflationary pressures, and supply chain disruptions.

One of the largest integrated worsted fabric producers in Europe, Yünsa has a strong global footprint. The company controls various stages of the production process, potentially offering advantages in terms of quality control and efficiency. However, it is also exposed to risks across the entire supply chain.

The company faces the critical challenge of adapting its business model to navigate the current economic climate. This involves implementing measures to reduce operational expenses and improve efficiency, exploring new product lines or markets to reduce reliance on specific segments, collaborating with suppliers and customers to enhance supply chain resilience, closely monitoring market trends and adjusting production accordingly and modernizing equipment and processes to improve productivity and reduce costs.